We no longer support this browser. Using a supported browser will provide a better experience.

Please update your browser.

With a GDP of $501 billion, the San Francisco metropolitan area is the sixth largest economy in the U.S. and an important hub in the global economy.1 The median household income in San Francisco is $96,265 and there are 99,307 small, non-employer establishments.2 Moreover, the unemployment rate is more than a percentage point lower than the country as a whole and average hourly wages are $10 more than the national average.3 While the overall economy in San Francisco is strong, there is significant variation in household and small business financial outcomes.

To better understand the financial lives of U.S. households and small businesses, the JPMorgan Chase Institute explored questions of economic relevance through the lens of de-identified transaction and account summary data from over 70 million consumers and 2.5 million small businesses. These data allowed us to provide localized insights on the San Francisco economy, including trends in out-of-pocket healthcare spending, Online Platform Economy participation and revenues, local commerce, and small business financial outcomes. Our local commerce and Online Platform Economy data allow us to observe trends at the San Francisco metropolitan area level, whereas our small business data are aligned to San Francisco city limits, and our healthcare research observes trends at the county level.

American households experience significant income and expense volatility. The Online Platform Economy has created a new marketplace for work by providing flexible, highly accessible opportunities to generate earnings that have the potential to help individuals buffer against income and expense shocks. JPMorgan Chase Institute research has divided the Online Platform Economy into four key sectors: transportation, leasing, selling, and non-transport work. In the JPMorgan Chase Institute report, The Online Platform Economy in 27 Metro Areas: The Experience of Drivers and Lessors, we leveraged de-identified data from 2.3 million families participating in the Online Platform Economy to track supply-side participation, revenues, and engagement rates in two sectors—transportation and leasing—across 27 metro areas.

We observed strong secular national trends in two of the sectors, transportation and leasing, starting in 2013. Nationwide, transportation sector participation—measured as the fraction of our sample generating income through a transportation platform in any given month—increased by more than a factor of 20 from 2013 to 2018, while average monthly revenues declined by half. On the leasing side, we found that participation rates tripled nationwide while average monthly revenues doubled.

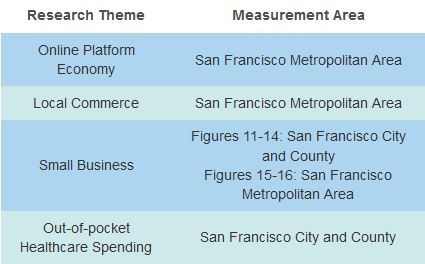

These national trends tell a story that is consistent across many metro areas. In the transportation sector, average revenues fell by 40 percent or more in 15 metro areas and did not increase in any metro area, whereas participation rates increased in every area we tracked. In San Francisco, transportation sector participation increased from 0.17 percent in the first ten months of 2013 to 1.85 percent in the first ten months of 2018, and average driver revenues decreased by 27 percent from $1,696 in the first ten months of 2013 to $1,231 in the first ten months of 2018. In seven cities, there were too few participants in 2013 to present the area average, and so those are rolled into the residual group which we label “Everywhere Else.”

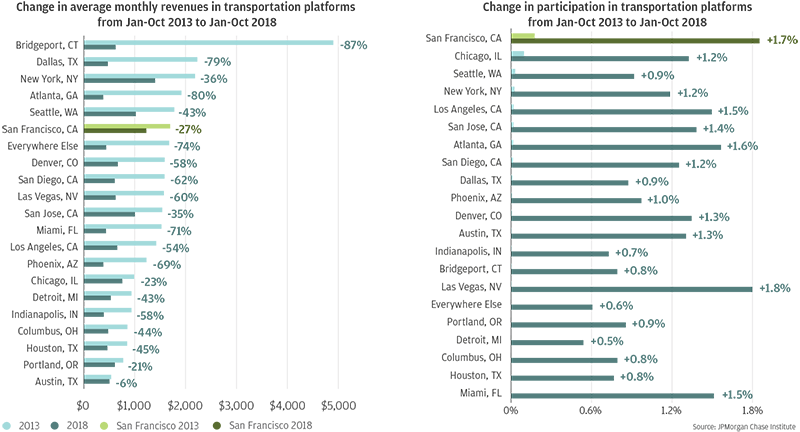

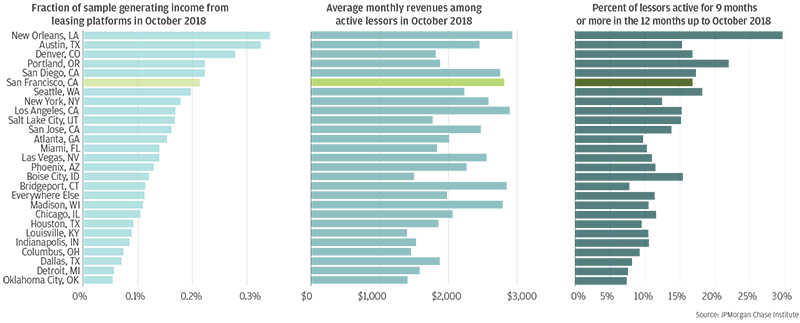

On leasing platforms, participation rates increased in every area, while average monthly lessor revenues doubled or more in 21 areas and increased in all 28. In San Francisco, leasing participation doubled from 0.11 percent in the first ten months of 2013, to 0.22 percent in the first ten months of 2018.

Along with these strong secular trends, we found that there is significant variation across cities at any point in time. Specifically, we looked at differences in participation rates, average monthly revenues, and engagement rates in October 2018. We defined engagement as the fraction of October 2018 participants who also earned platform income in eight or more months over the previous year. We focused on the month of October because it typically does not display a seasonal peak or trough in terms of income or spending. In the transportation and leasing sectors, we found that participation and revenues were positively correlated, but there were telling exceptions to that pattern.

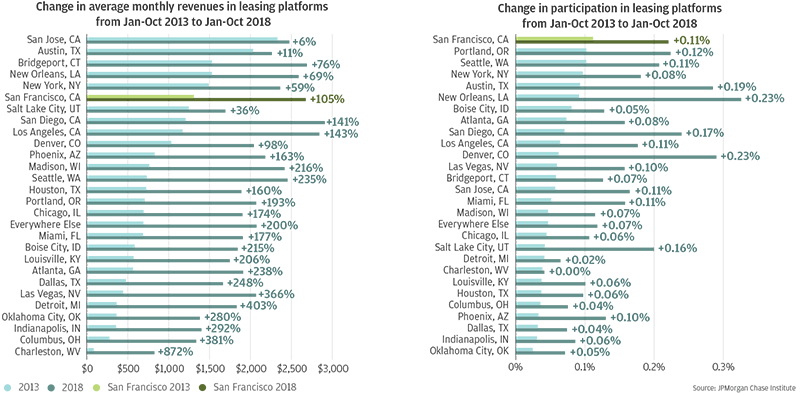

In the transportation sector, San Francisco had the highest driver participation—just under two percent—and had the highest revenues of any metro area ($1,508 per driver in October 2018). We found that patterns in engagement reflect patterns in revenues; San Francisco had one of highest engagement rates at approximately 15 percent.

Participation on leasing platforms is limited, but there is still significant variation across areas in terms of average monthly lessor revenues and engagement rates. In October 2018, San Francisco had comparatively high average monthly lessor revenues ($2,812 per lessor), moderately high participation (0.21 percent), and high engagement (about 17 percent).

Interestingly, San Francisco’s average driver and lessor revenues stood out for being significantly higher than other cities with similar participation rates in October 2018. Several supply- and demand-side factors are likely to play a role in explaining why particular cities stand out from the overall pattern, including regulation, vehicle ownership, hotel occupancy rates, and metro area density.

We found that metropolitan areas with larger incumbent industries as the Online Platform Economy emerged had higher participation and higher average revenues in the corresponding platform sectors. The measure of incumbent industries provides an indicator of the potential market size for new transportation and leasing service providers, thereby pointing at the demand side of the Online Platform Economy. Additionally, every local characteristic we explored that was associated with higher levels of participation was also associated with higher average monthly revenues. This suggests that rising participation does not directly cause falling average revenues, which are two coincident trends we observed in prior research.

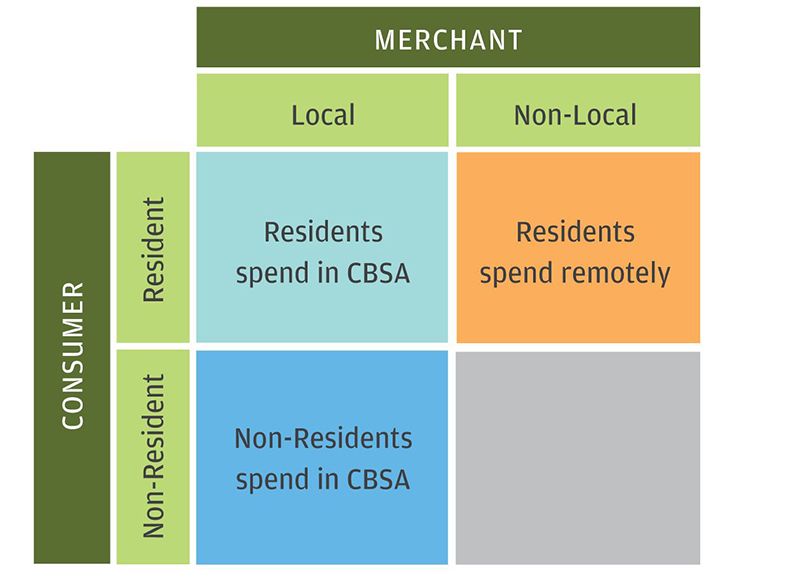

Consumer spending makes up more than two thirds of GDP.4 The JPMorgan Chase Institute’s Local Commerce research provides insights into the decisions made by consumers and businesses as measured by everyday debit and credit card purchases. By leveraging our Local Commerce (LC) lens, we provide a granular, transaction-level view into the demographic and firmographic drivers of spending growth in 14 U.S. cities. Moreover, we use customer and merchant location to understand the distance at which a purchase was made. With respect to spending growth, we generate two complementary views:

We leverage the merchant and consumer views of local spending to observe year-over-year growth in San Francisco, as well as demographic trends.

The Local Commerce Lens is framed along customer location, merchant location, and transaction channel. These dimensions lead to six different groups of transactions. The customer and merchant location determine the spatial distance at which the transaction occurred, while the online/offline channel determines to what extent the distance between the consumer and merchant matters.

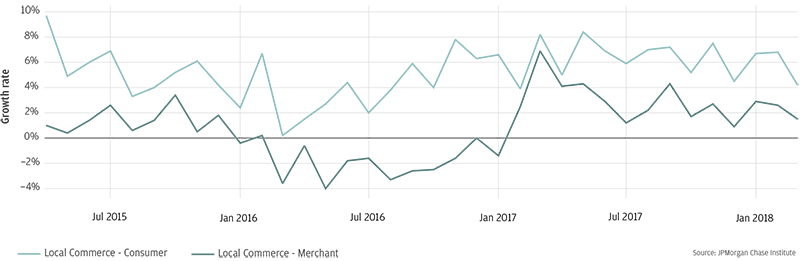

Comparing the topline year-over-year (YOY) growth rates in spending across the consumer and merchant lenses reveals that, in every month, spending by San Francisco residents grew faster than spending at San Francisco establishments. As noted in Box 1, spending by residents includes residents’ spending at establishments in other locations, while spending at San Francisco establishments includes purchases from residents of other localities. Insofar as spending by residents (consumer view) is increasing faster than spending at establishments (merchant view), the gap in growth rates highlights the role of remote purchasing (e.g. online commerce) as a large and growing component of San Francisco residents’ everyday spending behaviors, especially in comparison to locally-based spending.

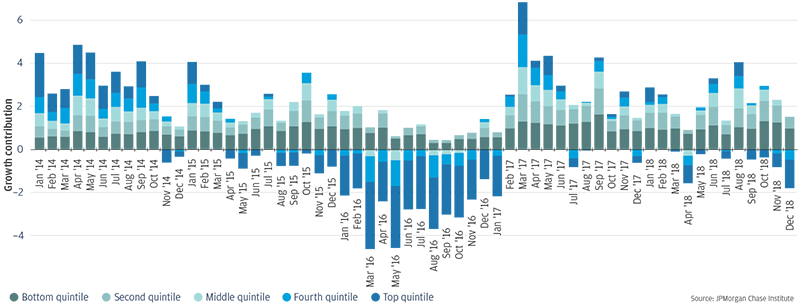

While the overall growth figures provide a high-level view of the vibrancy and overall health of the San Francisco economy, disaggregating this growth by customer and establishment characteristics provides crucial context and detail on which groups of people and businesses are contributing to overall growth. Figures 6-10 examine growth in San Francisco by characteristics presented in the merchant view of everyday spending found in the Local Commerce Index.

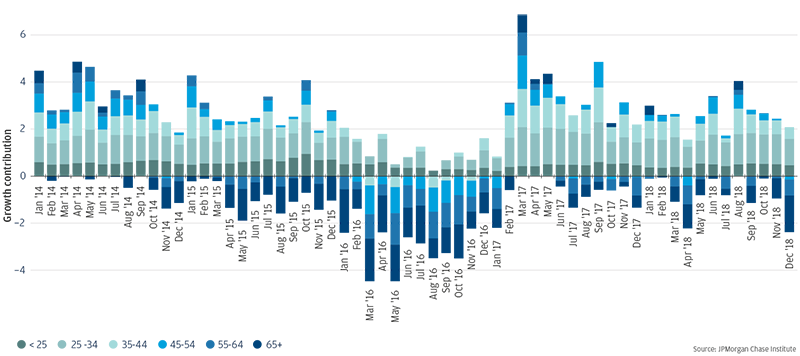

In San Francisco, younger consumers under the age of 35 tended to contribute more to growth compared to their older counterparts. Over the course of the series, consumers under 35 contributed an unweighted average of 1.5 percentage points to an unweighted average topline growth number of 1.5 percent.

Throughout the lifespan of the series, consumers under the age of 35 have never subtracted from spending growth in San Francisco. This highlights the important role that younger consumers have in driving spending growth at local merchants.

Similar to age, consumers on the lower end of the income spectrum tend to contribute the most and most consistently to growth. In fact, consumers in the first two income quintiles combined have never subtracted from growth. Over the course of the series, consumers in the first two income quintiles contributed an unweighted average of 1.4 percentage points to an unweighted average topline growth number of 1.5 percent.

In particular, consumers in the first income quintile have contributed the most to spending growth at San Francisco merchants 50 out of the 60 months we observe in our series, the most number of times of any income quintile.

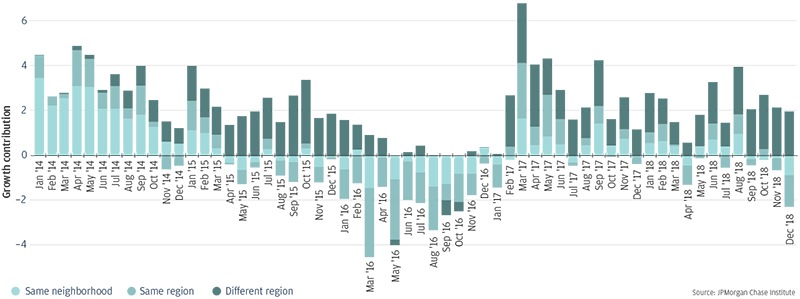

In the Local Commerce Index, spending by residents that live in the same Public Use Microdata Area as the establishment is considered “Same Neighborhood” spending. Relatedly, spending from other San Francisco residents and spending from consumers that live outside of San Francisco are considered “Same Region” and “Different Region” spending, respectively. The location of the consumer relative to the merchant gives a sense of the extent to which the growth (or decline) in spending remains in the community.

In San Francisco, we observe that contributions to spending growth mostly come from transactions in which the consumer was from a different region than the merchant. Over the course of the series, spending by those consumers from a different region than the merchant contributed an unweighted average of 1.2 percentage points to an unweighted average topline growth number of 1.5 percent.

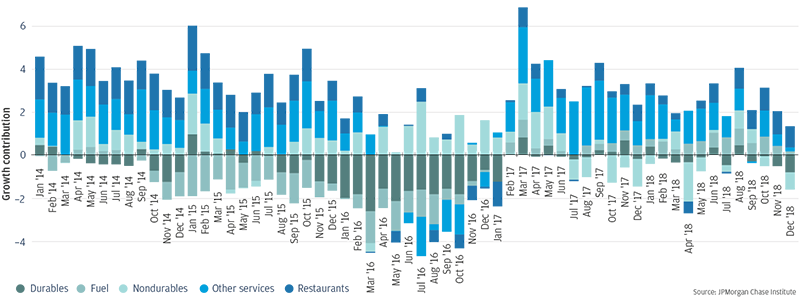

In San Francisco, spending at providers of other services (e.g. medical providers, accountants, professional services) tended to contribute the most to growth. Over the course of the series, spending at other services providers contributed an unweighted average of 1.1 percentage points to an unweighted average topline growth number of 1.5 percent.

Following other services providers, substantial contributions to growth were made by spending at restaurants and non-durables (e.g. groceries, clothing) providers, each contributing an unweighted average of 0.7 and 0.4 percentage points to overall growth over the course of the series, respectively.

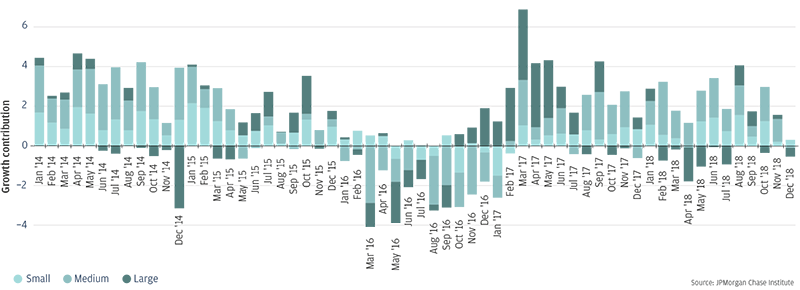

Looking at firm size, the spending growth contributions by small businesses play an important role in overall growth in San Francisco. Although medium-sized businesses contributed the most to growth the most number of times over the course of our series, it was small businesses that had the largest unweighted overall average growth contribution of 0.7 percentage points.

Spending at small businesses contributed an unweighted average of 0.7 percentage points to an unweighted average topline growth number of 1.5 percent over the course of the series. Spending at small businesses has been a nearly consistent contributor to overall growth, subtracting from overall growth only eight months in total.

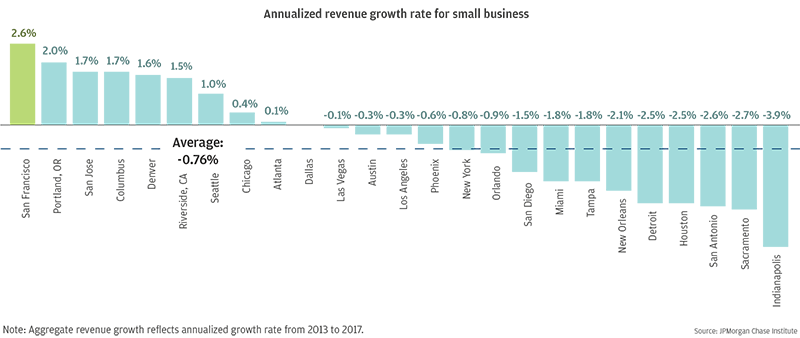

Small businesses are a pillar of urban economies, making substantial contributions to economic growth and dynamism. In the JPMorgan Chase Institute report, The Small Business Sector in Urban America: Growth and Vitality in 25 Cities, we analyzed differences in financial outcomes in the small business sector across some of the largest cities in the U.S., providing a lens into the composition and contributions of different types of firms to the aggregate revenue growth and exit rates of the small business sector. Our research leveraged deposit data from 290,000 small businesses that bank with Chase and suggested that small businesses in San Francisco are generally thriving.

Consistent revenue streams are critical for small businesses, fueling their ability to not only survive, but potentially grow. We found that the small business sector in San Francisco had the highest level of revenue growth compared to 24 other major U.S. cities, as the aggregate revenue of small businesses operating in San Francisco grew 2.6 percent annually over a period of four years.

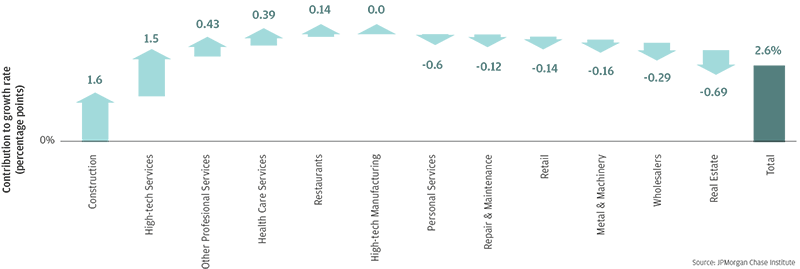

While the region’s reputation as a technology hub, relative to other cities we observed, still holds somewhat true for small businesses, small construction firms actually contributed the most to aggregate small business revenue growth in San Francisco, with small high-tech services firms second. Revenue growth contributions are net positive for restaurants (0.14 percentage points) and other professional services (0.43 percentage points), both of which had relatively high and sustained contributions to spending growth in our Local Commerce analysis.

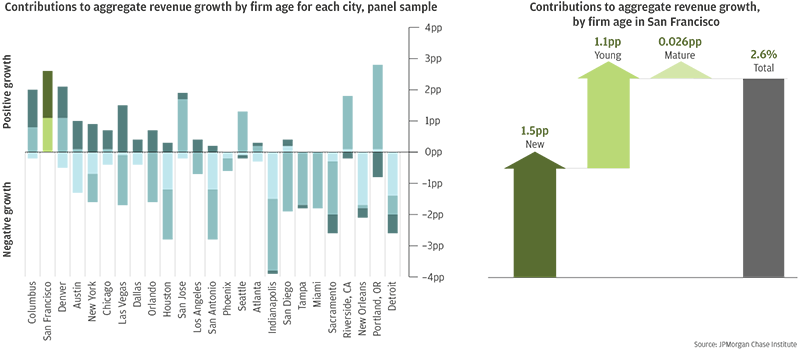

Moreover, our analysis showed that San Francisco was one of the few cities where both new firms (<1 year old) and young firms (1-10 years old) made positive contributions to growth. This suggests that vibrancy in the small business sector in San Francisco is not concentrated only among new firms but rather sustained across firms of all ages. However, new firms grew the fastest in San Francisco. New firms grew 9.8 percent annually, with most of this growth concentrated in the top five percent of firms as defined by their total dollar value change in revenue from 2013 to 2017.

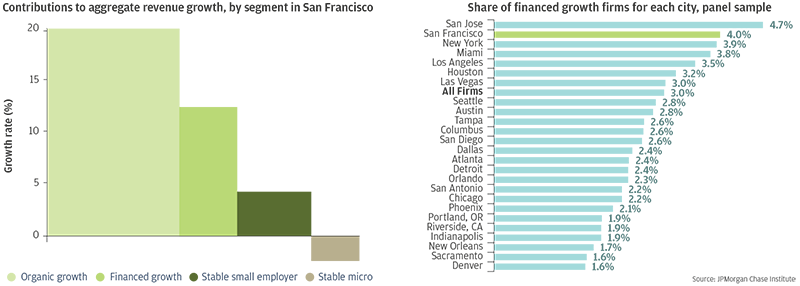

In the JPMorgan Chase Institute report Growth, Vitality, and Cash Flows: High-Frequency Evidence from 1 Million Small Businesses, we proposed a segmentation of small firms based on size, complexity and dynamism as a way to identify the contributions of different small business segments to the U.S. economy. In San Francisco, we found that organic growth firms, which are characterized by their intent to grow out of operating profits rather than the use of external financing, experienced the largest revenue growth. Moreover, within the top five percent of new firms, over 70 percent were organic growth firms. In contrast, stable micro firms, which are characterized by having no or very few employees, actually saw revenue declines. Additionally, while the share of financed growth firms is only three percent across the entire sample, some metro areas had a much higher concentration of these firms than others. More than four percent of all small firms in the San Jose and San Francisco metro areas were in the financed growth segment.

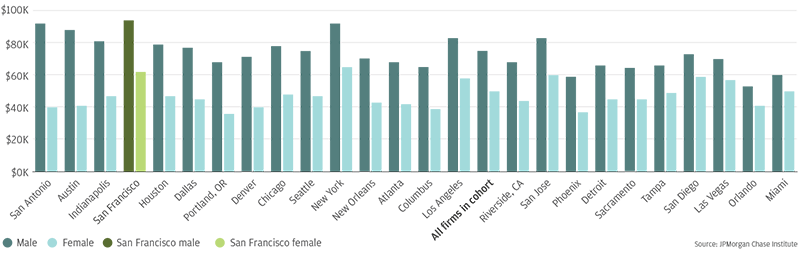

In our recent report, Gender, Age, and Small Business Financial Outcomes, we observed small business financial performance, with a specific emphasis on differences in outcomes by owner age and gender. Overall, female-owned firms generated median first-year revenues that were about 34 percent lower than median revenues of male-owned firms. Firms founded by women were smaller than firms founded by men in every metropolitan area, though the size differential varied by location. In San Francisco, female-owned firms had $62K first year revenues whereas male-owned firms generated $94K their first year.

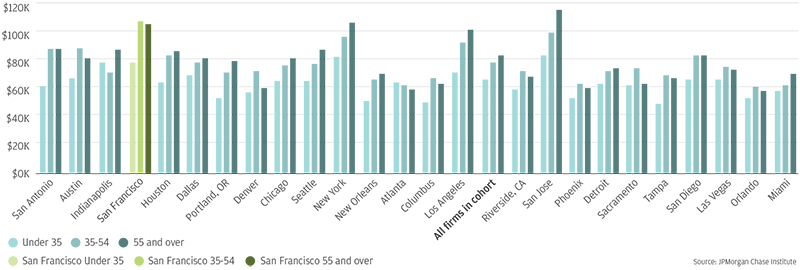

Additionally, we observed that young business owners under the age of 35 typically started smaller firms. In San Francisco, small business under 35 generated $78K in first-year revenues, whereas owners 35-54 generated $107K and owners 55 and over generated $105K.

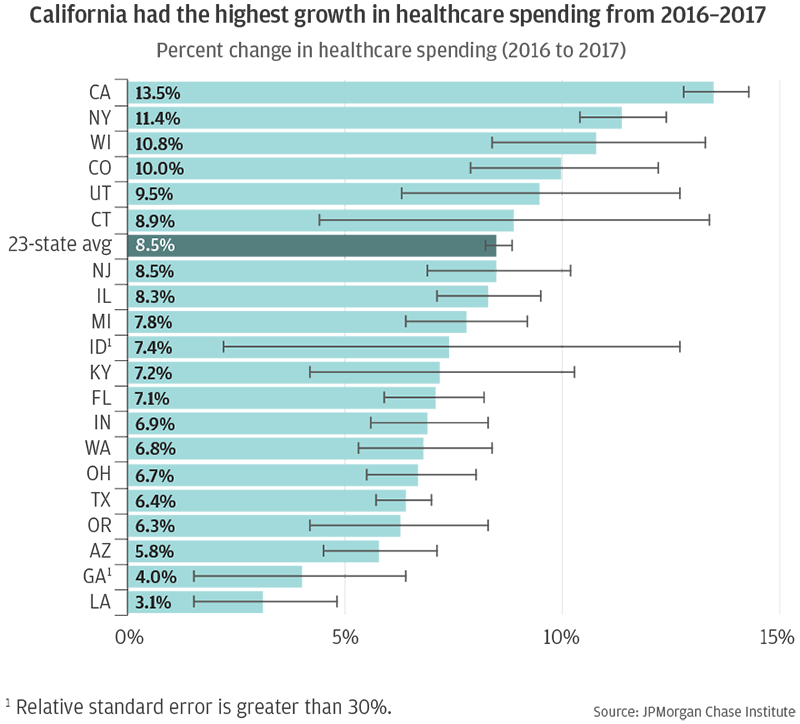

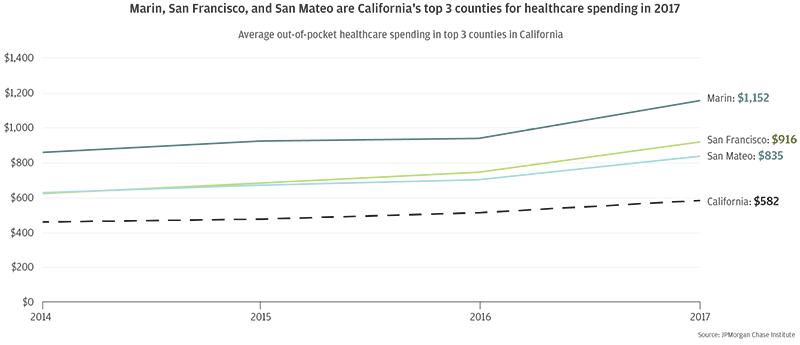

Healthcare spending is linked to families’ cash flows, and these dynamics affect not just when people pay for healthcare but also when they consume it. In the JPMorgan Chase Institute report, On the Rise: Out-of-Pocket Healthcare Spending in 2017, we explored families' out-of-pocket healthcare expenditures and the financial burden they imposed on families over time. Of the 23 states we tracked, California showed the fastest growth in spending levels from 2016 to 2017. The high healthcare spending growth in California in 2017 holds true across different demographics groups, indicating that all sub-populations experienced roughly comparable increases in out-of-pocket healthcare expenditures.

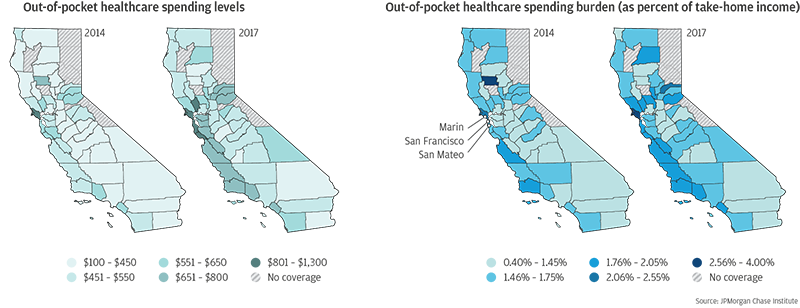

Top-spending counties in California tended to be high-income and located along the coast, especially in the Bay Area. The top three counties in terms of spending levels were Marin, San Francisco, and San Mateo, where the average annual growth rates exceeded ten percent from 2014 to 2017. In fact, there were a total of 13 counties in California that had average annual growth exceeding ten percent during this time period. High-income groups generally tended to spend more on healthcare. These coastal areas in California have high income and high costs of living, which may translate to high county averages in healthcare spending, leading to the geographic gradient we observed in county-level maps. However, it is noteworthy that the growth in these high-income counties exceeded the growth in spending across the 23 states we observed even among the high-income group. This underscores that these coastal regions in California, including San Francisco, have experienced considerable growth in healthcare spending during the last few years and especially in 2017.

These insights provide a multi-faceted view of the financial health of San Francisco residents and small businesses.

Our geographically granular view of household spending can measure economic vibrancy and highlight local fiscal dynamics. Local leaders can use these data to better understand the economic activity of their jurisdiction, as well as how the locus of economic activity is changing over time. Additionally, our data provide a lens into small business aggregate revenue growth and exit rates—two key dimensions that characterize the economic health of the small business sector across cities. To the extent that there are specific and transferrable small business programs or policies that enable growth without impairing survival in cities, San Francisco could serve as a useful model given its relatively high small business revenue growth rates compared to exit rates.

We thank Bryan Kim, Tanya Sonthalia, and Chex Yu for their research assistance and thoughtful contributions to this work.

This effort would not have been possible without the diligent and ongoing support of our partners from the JPMorgan Chase Consumer and Community Bank and Corporate Technology teams of data experts, including, but not limited to, Howard Allen, Samuel Assefa, Connie Chen, Anoop Deshpande, Andrew Goldberg, Senthilkumar Gurusamy, Derek Jean-Baptiste, Joshua Lockhart, Ram Mohanraj, Ashwin Sangtani, Stella Ng, Subhankar Sarkar, and Melissa Goldman, as well as JPMorgan Chase Institute team members, including Elizabeth Ellis, Alyssa Flaschner, Courtney Hacker, Sarah Kuehl, Caitlin Legacki, Sruthi Rao, Carla Ricks, Tremayne Smith, Gena Stern, Maggie Tarasovitch, Preeti Vaidya, Marvin Ward, and Chris Wheat.

Finally, we would like to acknowledge Jamie Dimon, CEO of JPMorgan Chase & Co., for his vision and leadership in establishing the Institute and enabling the ongoing research agenda. Along with support from across the firm—notably from Peter Scher, Max Neukirchen, Joyce Chang, Patrik Ringstroem, Lori Beer, and Judy Miller—the Institute has had the resources and support to pioneer a new approach to contribute to global economic analysis and insight

JPMorgan Chase & Co.'s website terms, privacy and security policies don't apply to the site or app you're about to visit. Please review its website terms, privacy and security policies to see how they apply to you. JPMorgan Chase & Co. isn't responsible for (and doesn't provide) any products, services or content at this third-party site or app, except for products and services that explicitly carry the JPMorgan Chase & Co.