We no longer support this browser. Using a supported browser will provide a better experience.

Please update your browser.

In 2016 the metropolitan share of US Gross Domestic Product was nearly 90 percent. Given the large share of economic output from metropolitan areas it is critical for stakeholders, researchers, and policymakers to have granular, high-frequency economic measurement and analyses at the metropolitan level to complement existing local economic research.

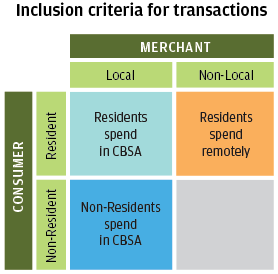

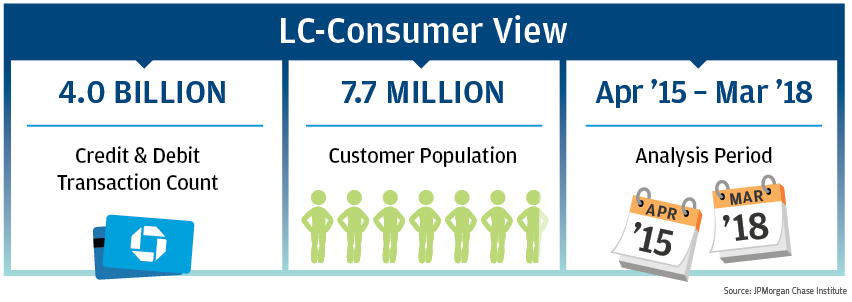

In this report, the JPMorgan Chase Institute expands the scope of our Local Commerce (LC) analyses through the introduction of our consumer view – namely, the transactions executed by consumers residing within a given metro area. This view complements the merchant view leveraged in our existing Local Commerce Index which examines the transactions executed at merchants located within a given metro area. The consumer view enables exploration of the extent to which online commerce has affected growth, who has driven that growth, and how it has impacted the offline marketplace.

The JPMorgan Chase Institute frames the Local Commerce lens along three dimensions:

Customer and merchant locations allow us to understand the extent to which customers are shopping at local merchants versus merchants that are located in different metro areas. The transaction channel allows us to understand whether or not the purchase was a made at a distance.

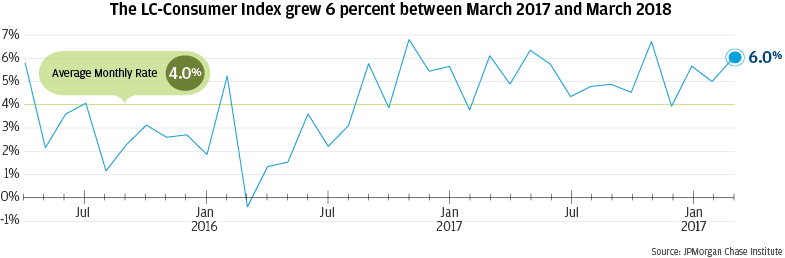

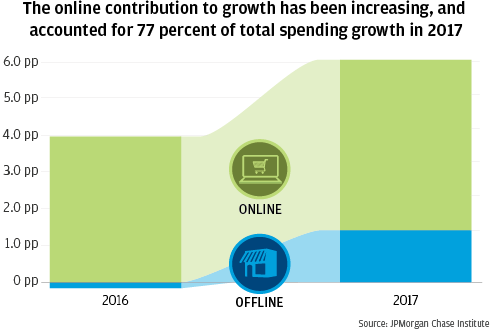

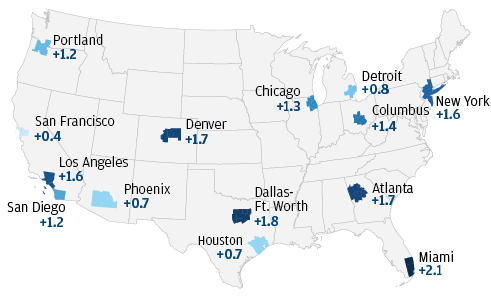

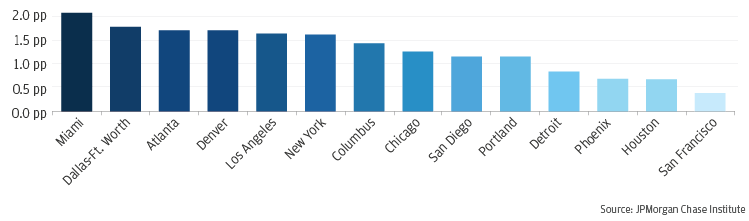

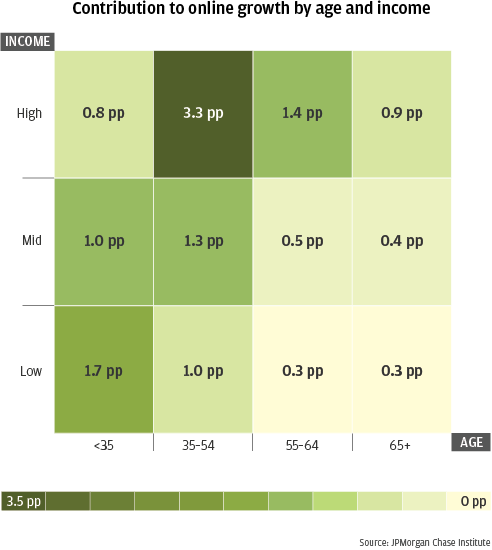

The consumer view of Local Commerce provides a granular view of online spending and its implications for local economies that is difficult to capture via other data sources. Our initial analysis has revealed that the growth rate for online spending is highest for lower income customers under 35, but the largest contributions to growth come from the high-income 35-54 year olds. High and growing shares of LC-Consumer spending take place online and this is true across all metro areas we tracked. This growth in online spending has been accompanied by an increase in spending at merchants that are located outside the metro area of the consumer. The implications of these changes for local economies are not yet clear, but the LC-Consumer Index can provide unprecedented insight into an evolving commerce landscape.

JPMorgan Chase & Co.'s website terms, privacy and security policies don't apply to the site or app you're about to visit. Please review its website terms, privacy and security policies to see how they apply to you. JPMorgan Chase & Co. isn't responsible for (and doesn't provide) any products, services or content at this third-party site or app, except for products and services that explicitly carry the JPMorgan Chase & Co.