We no longer support this browser. Using a supported browser will provide a better experience.

Please update your browser.

The Great Recession brought to the forefront many unanswered questions about how monetary policy plays out at a microeconomic level, notably the question of how changes in the federal funds target rate impact personal consumption for individual households. Not surprisingly, this question is difficult to answer because of the multitude and variety of financing products and constantly evolving market conditions, as well as the paucity of data integrating financing terms with consumption at the household level over time. In this new JPMorgan Chase Institute report, we turn to a sample of homeowners who hold a specific type of mortgage particularly sensitive to interest rate changes to inform this question in an innovative way.

We examine how a sample of US homeowners changed their credit card spending in response to a predictable drop in their mortgage payment driven by the Federal Reserve’s low interest rate policy that followed the Great Recession. Using a de-identified sample of Chase customers who had hybrid adjustable-rate mortgages (ARMs) and a Chase credit card, we analyze changes in credit card spending and revolving balance leading up to and after mortgage reset.

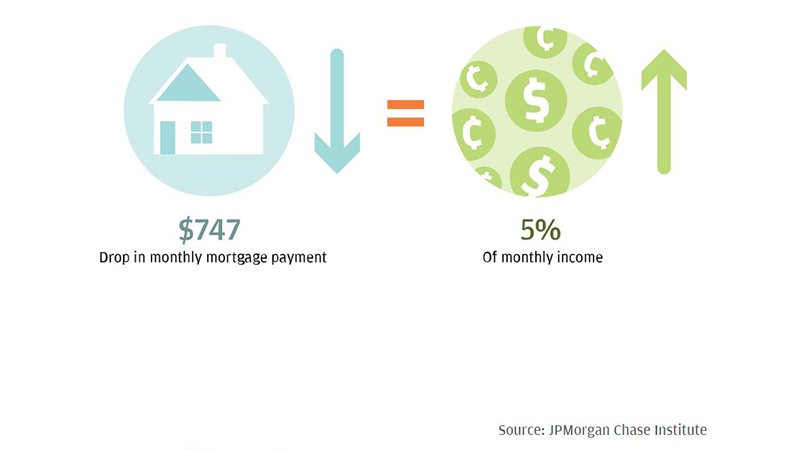

The 44 percent of homeowners in our sample that had a mortgage with a stable amortization schedule realized an average of $747 in monthly savings upon reset. Against their average monthly income of $13,834, this savings was equivalent to an income boost of over 5 percent.

Housing wealth declined for this group: between origination and reset, the median home value for this cohort dropped by nearly $84,000 (25 percent).

Over the 12 months preceding ARM reset, credit card spending increased by 9 percent ($289 per month) on average relative to spending in the baseline month (12 months before reset). Importantly, this spending occurred prior to any decrease in mortgage payment, and thus was an anticipatory response. Over the 12 months after reset, spending increased by 15 percent ($488 per month) on average relative to spending in the baseline month.

These homeowners increased their spending despite a nearly $84,000 (25 percent) drop in their median home value and associated rise in loan-to-value ratio, indicating that the decrease in housing wealth and ensuing increase in household leverage did not prevent them from increasing their spending in response to a boost in income.

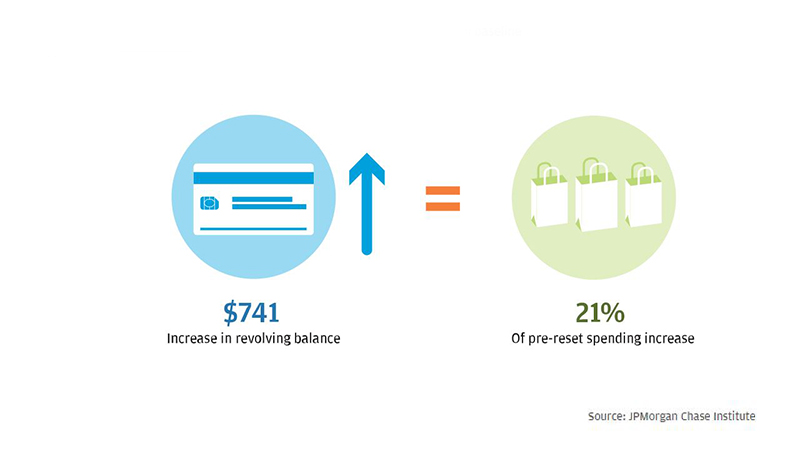

On average, homeowners in our sample used $741 of credit card borrowing in the pre-reset period to smooth the increase in their consumption before income actually increased. The $741 increase in revolving balance suggests they financed 21 percent of their pre-reset spending increase.

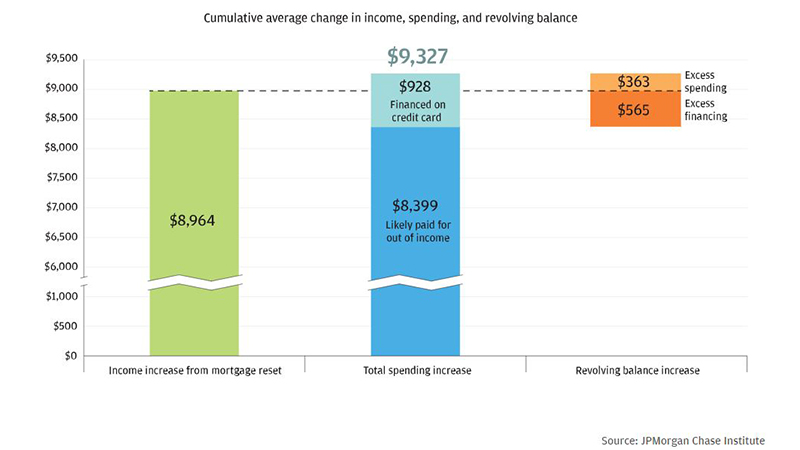

Over the full two-year period, the average revolving balance increased by $928 and the total spending increase actually exceeded the total savings from mortgage reset by 4 percent ($363). Comparing the $928 increase in revolving balance to the $363 of excess spending suggests that these households could have reduced their revolving balances by $565 at the end of the period without changing their credit card spending levels over the prior 24 months.

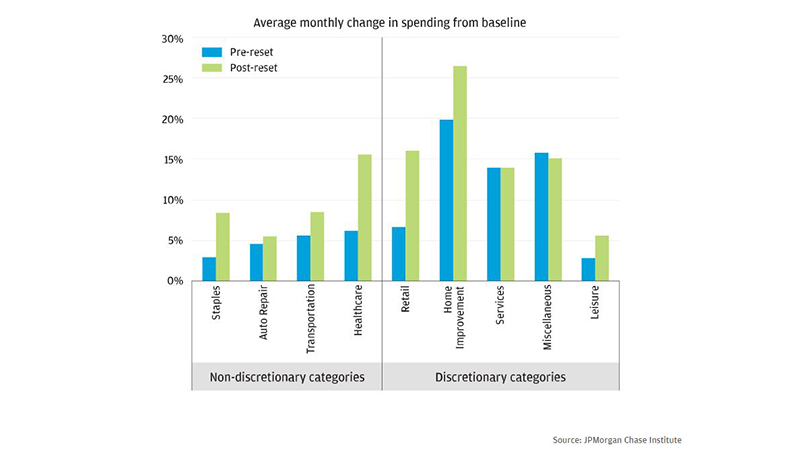

In both the pre-reset and post-reset periods, spending increased in every category and the discretionary spending increase exceeded the non-discretionary spending increase.

Within discretionary purchases, spending on home improvements increased the most. This is particularly noteworthy as it represents an increased investment in a leveraged asset just after the asset lost 25 percent of its value.

Within non-discretionary purchases, spending on healthcare increased substantially but only in the post-reset period, suggesting homeowners postponed healthcare expenditures until the income increase materialized.

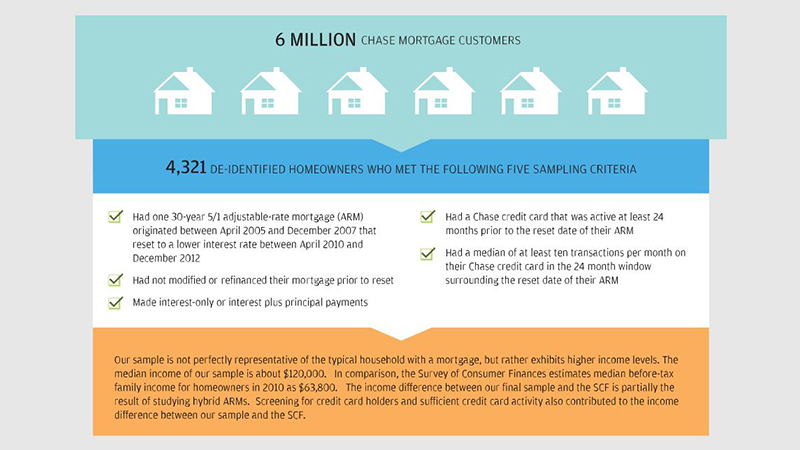

From a universe of over 6 million Chase mortgage customers, we created a sample of 4,321 de-identified homeowners who met the following five sampling criteria:

Monetary policy affects the economy through many channels, and the effectiveness of each channel varies in easing and tightening cycles. In this report we measure the effects of the income channel of monetary policy on the consumption of homeowners with a specific type of variable-rate mortgage. We find that in a declining interest rate environment, the income channel is automatic, the consumer response is considerable, and that there are both anticipatory and contemporaneous increases in consumption. To put our findings in the broader context of the monetary policy transmission channels that operate through mortgages to impact personal consumption, we turn to research that shows that the refinancing channel suffers from shortcomings that limit its impact on homeowners: it is difficult to activate with conventional interest rate policy, has frictions that reduce its bandwidth, and has uneven distributional effects.

Importantly, housing policy that influences the share of fixed-rate mortgages versus variable-rate mortgages will partially determine the share of homeowners that will be impacted by the refinancing channel versus the income channel and therefore will also impact the overall effectiveness of monetary policy. As such, when housing policy makers evaluate the policies that influence which type of mortgage (fixed-rate or variable-rate) borrowers choose, they should consider the effects these policies will have on the ability of monetary policy to impact personal consumption through the business cycle.

JPMorgan Chase & Co.'s website terms, privacy and security policies don't apply to the site or app you're about to visit. Please review its website terms, privacy and security policies to see how they apply to you. JPMorgan Chase & Co. isn't responsible for (and doesn't provide) any products, services or content at this third-party site or app, except for products and services that explicitly carry the JPMorgan Chase & Co.