We no longer support this browser. Using a supported browser will provide a better experience.

Please update your browser.

When a family experiences a cash flow interruption, they can adjust by borrowing, cutting expenditures, or generating supplementary income. With the rise of the Online Platform Economy, this last option has likely become more available.

When a family experiences a cash-flow interruption, they can adjust by spending down savings, borrowing, cutting expenditures, or generating supplementary income. With the rise of the Online Platform Economy, this last option has likely become more available. In this study, we report that supply-side participation in the Online Platform Economy functions as a cash-flow management tool for many families.

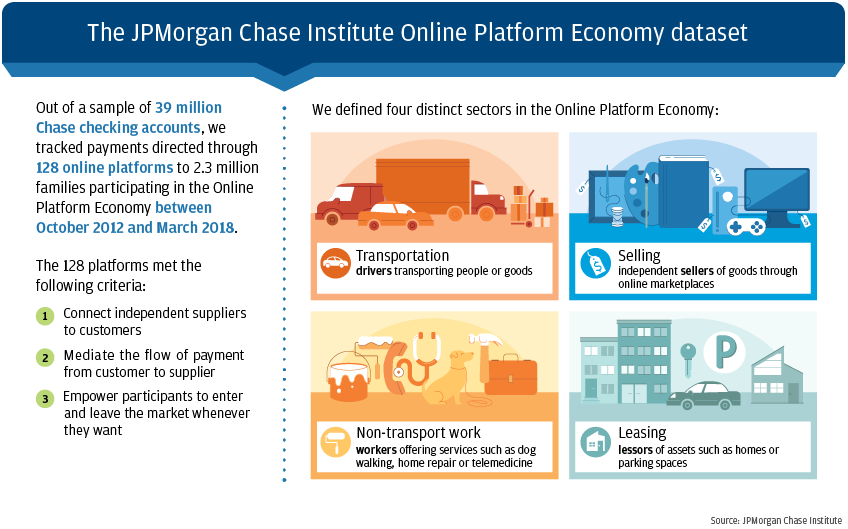

We leverage the JPMorgan Chase Institute Online Platform Economy data set to investigate whether and how families use the Online Platform Economy to smooth income. We do this by taking two converse perspectives. First, we track the evolution of income and cash balances in the weeks leading up to and immediately following a family’s first joining the Online Platform Economy. Conversely, we then track how Online Platform Economy participation rates and average weekly platform revenues evolve around discrete cash-flow events. In total, we analyze five specific events occurring in the years 2016 and 2017:

Average cash balances and average weekly take-home payroll income remain roughly constant until about ten weeks before a family begins participating in the Online Platform Economy. Then, both begin to decline in tandem, implying that families may be using liquid balances to maintain their expenditures while missing payroll income. About two weeks before joining the Online Platform Economy, average cash balances and payroll incomes are down almost 10 percent. Income from government sources (including, for example, social benefits like unemployment insurance) begin to decline twenty weeks before joining, but fall most sharply in the final ten weeks.

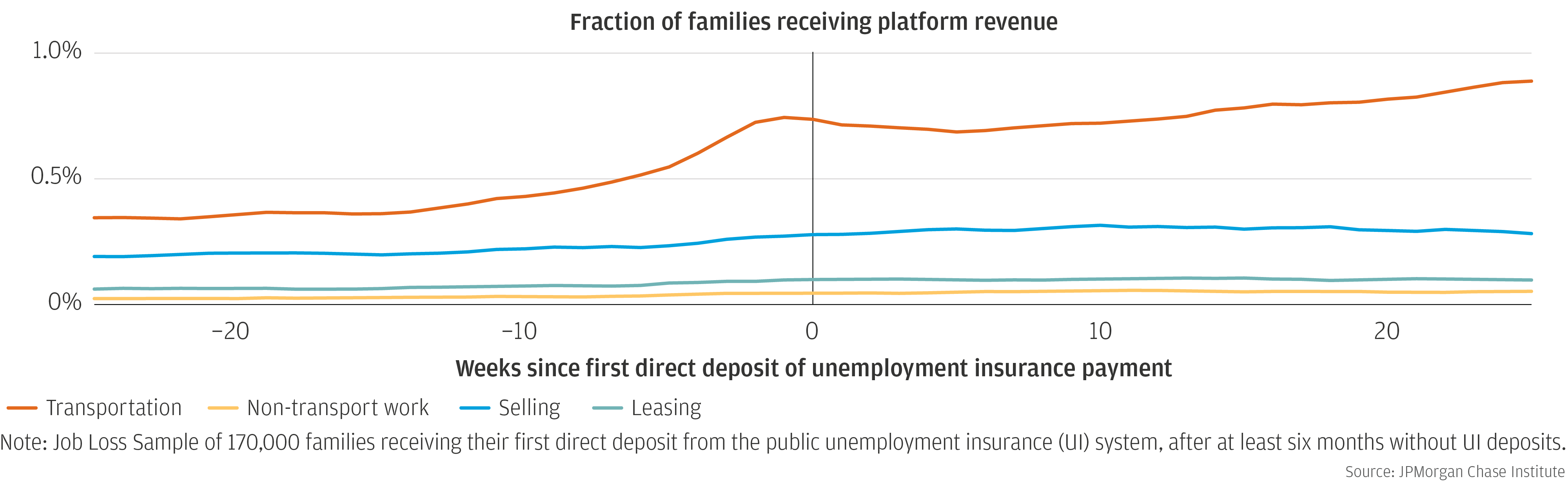

In the wake of an involuntary job loss, many families turn to transportation platforms to supplement their income, and some also begin selling assets. Transportation platform participation rates increase from 0.43 percent to 0.74 percent around this event—an increase of 0.31 percentage points, or 72 percent. Participation rates on selling platforms increase from 0.22 percent to 0.28 percent—an increase of 0.06 percentage points, or 27 percent.

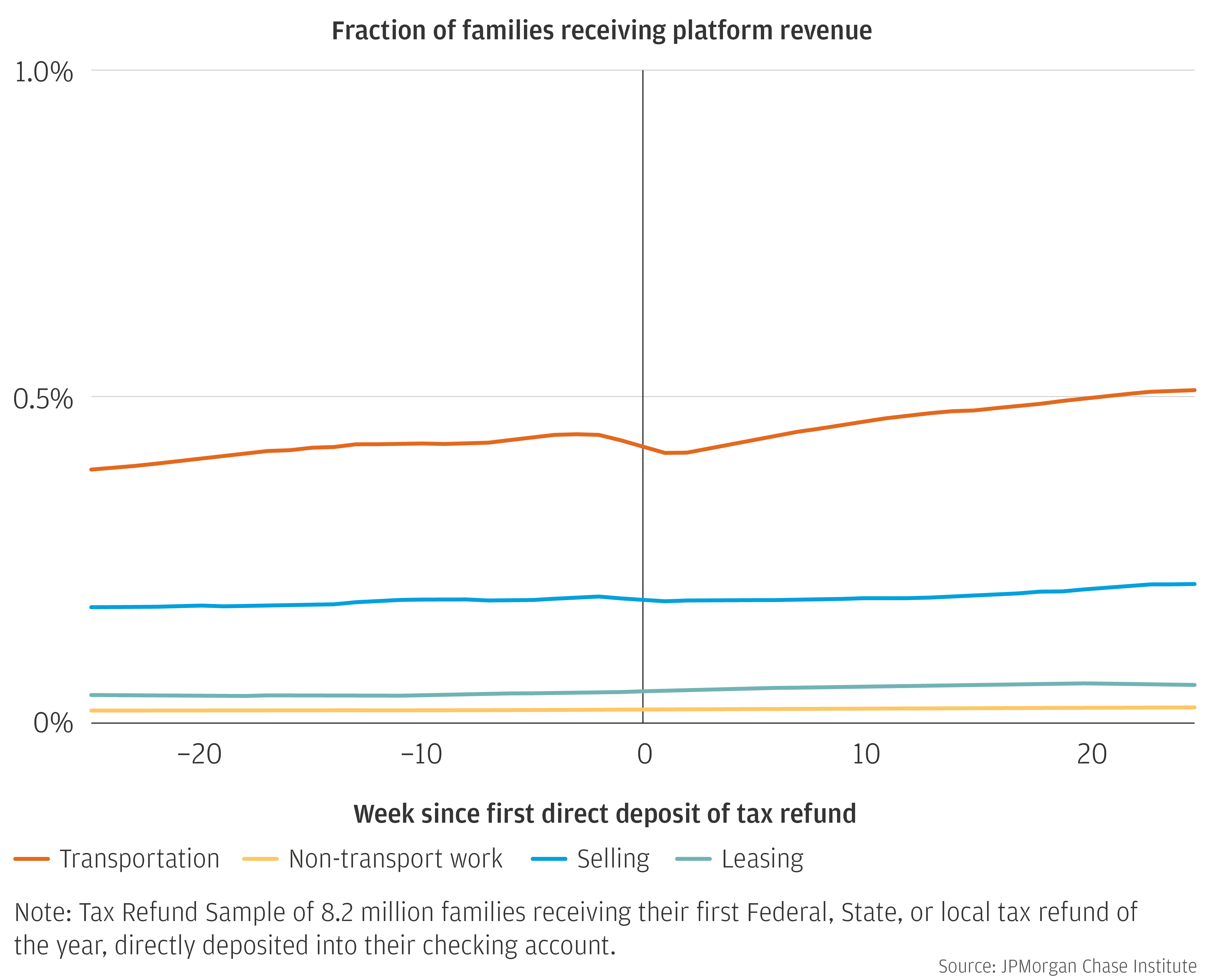

Tax refunds and tax payments do not catalyze changes in participation in the Online Platform Economy, other than a minor dip in driver participation in the week when a tax refund is received. Nor do families flex their engagement in response to these cash-flow events—for example, by using cash from a refund to buy back some leisure time.

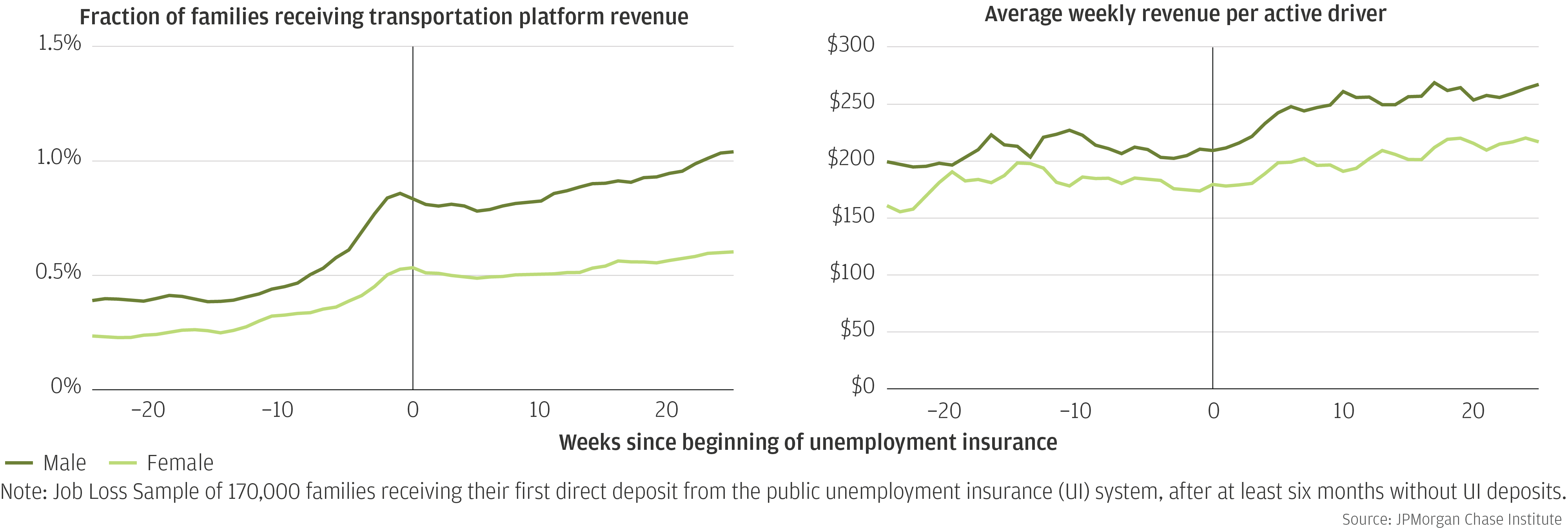

Families are more likely to turn to platforms to smooth income around an involuntary job loss if the primary account holder is a man. Regardless of gender, however, families turning to the Online Platform Economy during a spell of involuntary unemployment are most likely to join the transportation sector. Average revenues per driver, and the gender gap in those averages, remain stable in the weeks leading up to a first unemployment insurance payment. Notably, the gap increases to about $50 in the weeks after.

Taken together, our findings indicate that the Online Platform Economy—and particularly its transportation sector—play an income-smoothing function for families between jobs. However, the tax-related cash flow events do not coincide with changes in platform participation or revenues. These findings add an important dimension to discussions around the design of policy and regulation of these labor markets. We see four especially important implications:

First, as policymakers weigh approaches to improve the pay, benefits, and protections of platform workers, they ought to take into consideration potential impacts those same approaches might have on the very characteristics of platform work—low barriers to entry and high flexibility—that allows families to use it to smooth their income. Families in need of an income-smoothing tool may be turning to transportation platforms in particular because barriers to entry on these platforms may be lower than other sectors, and because it may be comparatively easy to generate revenues in the transportation sector with only occasional and periodic engagement. As policy discussions continue around portable benefits schemes, it is important to consider separately the needs of workers who intend to use platforms or other gigs as a primary source of income over the long-term from those who intend to use them as a temporary income-smoothing tool.

Second, the Online Platform Economy may be more available as an income-smoothing tool for some families than for others. Women (or family members who share accounts with women) experiencing interruptions to their payroll income are less likely to turn to the Online Platform Economy. To the extent that this difference may reflect structural disparities, it would require attention from both policymakers and platform providers.

Third, although fewer than 1 percent of families experiencing involuntary job loss actually turn to the Online Platform Economy to smooth their income, for those families the additional $150-$250 per week in platform revenues may be crucial. Fully accounting for the additional marginal costs associated with platform participation is likely difficult even for participants, so the extent to which platform participation is effective in generating real income remains unknown. However, the additional cash flow may address important immediate needs.

Finally, high rates of labor churn in the Online Platform Economy have been taken in some policy discussions as an indication that joining may have proved to be a bad financial decision for many drivers. However, our findings imply that one function driving through the Online Platform Economy may play is to bridge a gap between jobs. In that case, the fact that many drivers find another job and become inactive shortly after joining should not necessarily be interpreted as “voting with their feet” against the viability of the Online Platform Economy as an option for generating income.

JPMorgan Chase & Co.'s website terms, privacy and security policies don't apply to the site or app you're about to visit. Please review its website terms, privacy and security policies to see how they apply to you. JPMorgan Chase & Co. isn't responsible for (and doesn't provide) any products, services or content at this third-party site or app, except for products and services that explicitly carry the JPMorgan Chase & Co.