We no longer support this browser. Using a supported browser will provide a better experience.

Please update your browser.

Even amidst strong macroeconomic conditions, families experience high levels of income volatility that have important implications for well-being. Previous JPMorgan Chase Institute research has shown that families cut consumption on everyday necessities when they experience job loss, and delay spending on healthcare and durable purchases until their tax refund arrives. A key reason for this is that they have an insufficient liquid cash buffer. Families with limited liquid assets are dramatically less likely to smooth consumption in the face of income fluctuations.

It stands to reason then that racial gaps in liquid assets and wealth could result in racial differences in consumption smoothing. Longstanding gaps in income and wealth between White families and Black and Hispanic families have been well documented and have only grown following the Great Recession. What are the downstream consequences of these racial gaps in financial circumstances, particularly when families’ incomes fluctuate on a day-to-day and month-to-month basis?

This report provides a first-ever high-frequency look at racial gaps in liquid assets, take-home income, and families’ consumption response to income volatility from the vantage point of a novel de-identified data source: administrative banking data paired with self-reported race information. We matched Chase banking records with 2018 voter registration records in the states that had Chase branches in 2018 and that, under the Voting Rights Act, collect race information during voter registration.

This match yielded a large sample of 1.8 million families for whom we observe the race of the primary account holder along with other demographic characteristics, and a high-frequency, integrated view of income, spending, and liquid assets. This sample is broadly representative of the respective income distributions of Black, Hispanic, and White registered voters nationally and provides a reliable window into racial gaps in financial outcomes compared to benchmarks.

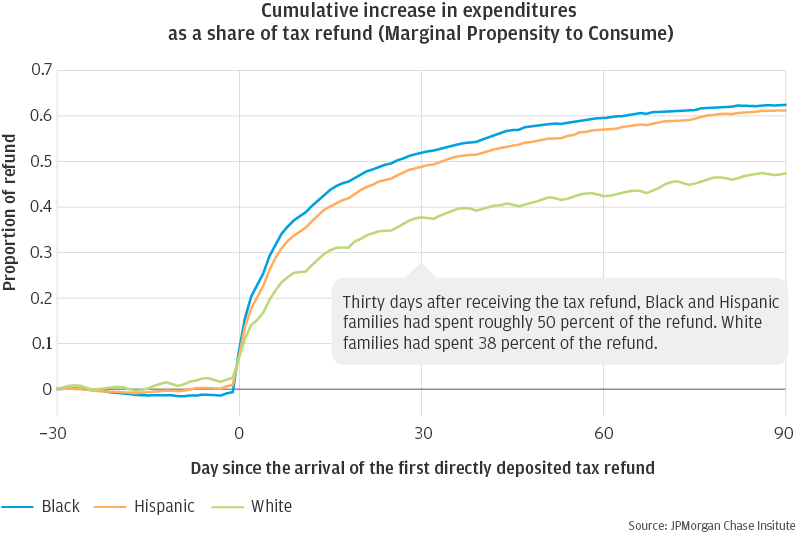

With this new data asset, we answer three key questions in this report. First, how large are the racial gaps in take-home income and liquid assets among Black, Hispanic, and White families and to what extent do they persist after accounting for other demographic factors? Second, are there racial differences in how much families smooth their consumption? We examine changes in everyday spending in response to two different sources of income volatility: involuntary job loss identified through the receipt of unemployment insurance benefits, a negative cash-flow event; and the arrival of a tax refund, a positive cash-flow event. Third, to what extent do racial gaps in liquid and financial asset buffers account for racial differences in families’ consumption response to job loss and tax refunds?

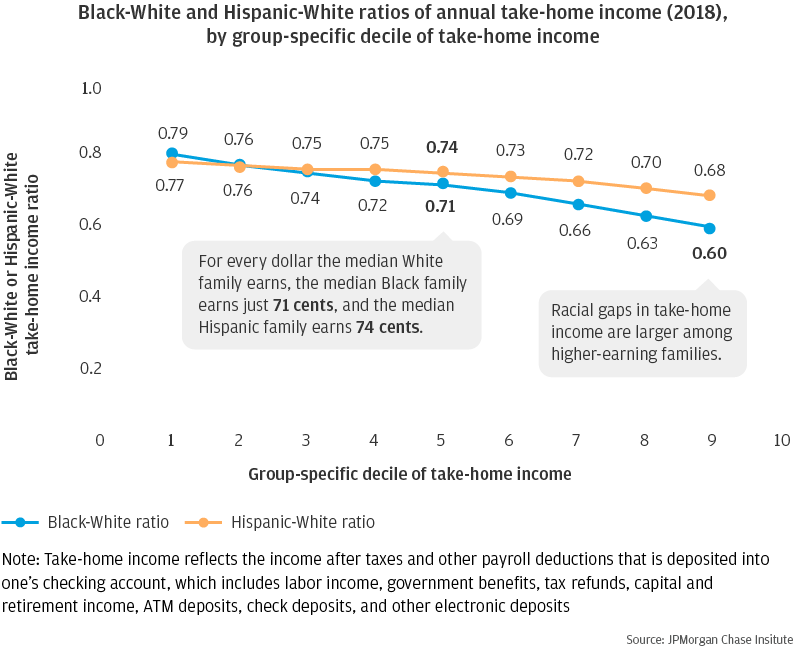

We measure the racial gap as the ratio of the take-home income for Black and Hispanic families, respectively, relative to White families, where race refers to the race of the primary account holder. Given that these measures are expressed as ratios, a ratio of 1.0 represents parity, and a lower ratio represents a larger racial gap.

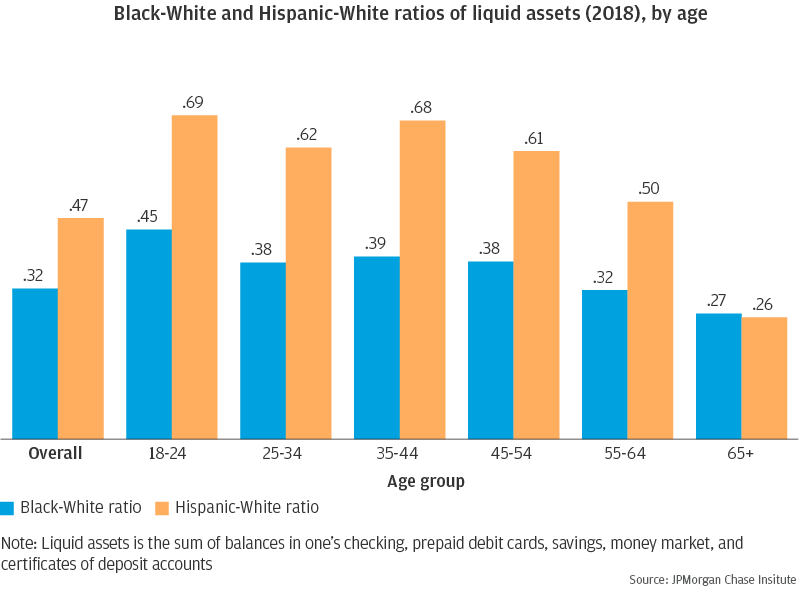

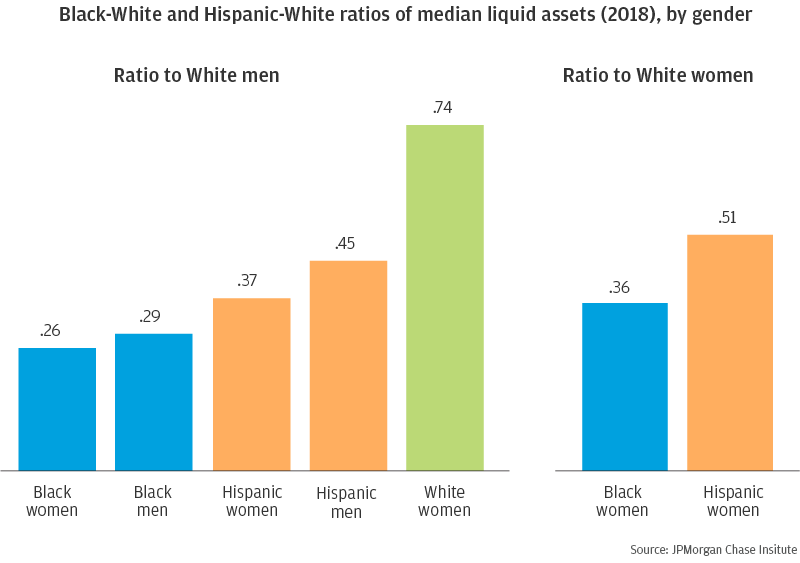

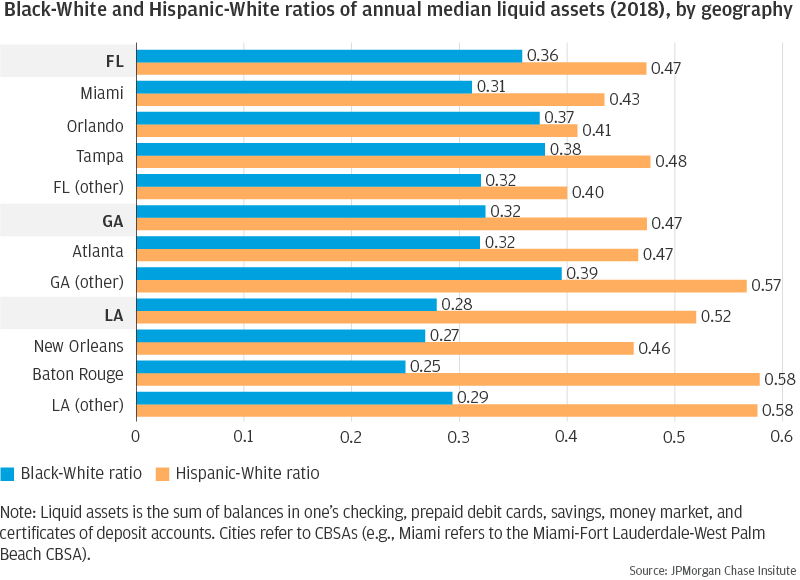

In conclusion, we find large racial gaps in take-home income and liquid assets which persist across age, income, gender, and geography. The racial gap in liquid assets makes Black and Hispanic families more vulnerable to income fluctuations. Families with lower liquid asset buffers—disproportionately Black and Hispanic families—cut their consumption to a greater extent when they experience involuntary job loss and increase their consumption to a greater extent when they receive a tax refund. However, racial gaps in consumption smoothing disappear when we account for the racial gaps in liquid and financial asset buffers.

These findings have important implications for public policy and the distributional impacts of policy interventions. They raise broader questions about how to reduce financial volatility and increase liquid assets for low-income families and, importantly, address the structural factors that contribute to racial gaps in income and assets.

Efforts to reduce income volatility, particularly among low-income families, may include expanding unemployment insurance benefits and ensuring access to workplace benefits and protections such as paid sick and family leave and a predictable work schedule. They could also include distributing tax credits and withholdings throughout the tax year.

In addition, we must consider ways to help families manage financial volatility. We estimate that a liquid asset buffer of roughly $5,000 to $6,000—as a form of “private insurance”—might enable Black and Hispanic families to sustain their typical consumption levels through a job loss or major cash-flow event. This is considerably more than the $1,000 to $1,500 that the median Black and Hispanic family in our sample currently has. Thus, a key question is how to support families in building these liquid assets.

Policies and programs that boost income and address the underlying challenges Black and Hispanic families face within the labor market could help to close racial gaps in income in the short-run. These could include increasing the minimum wage, strengthening the Earned Income Tax Credit, investing in job training programs, and reducing the barriers to employment for individuals with criminal backgrounds.

To close the racial gap in liquid assets, which is much larger, we also need stronger programs, policies, and innovations to both reduce expenses that disproportionately burden Black and Hispanic families and promote asset building among low-income families. These might include efforts to make housing, high-quality childcare, and higher education more affordable as well as employer- and government-sponsored supports for asset building.

The private, nonprofit, and government sectors all have important roles to play as policymakers, service providers, and employers in closing racial gaps in income and wealth. Our research shows the importance of disaggregating economic and financial statistics by race and measuring these statistics at a high frequency. Doing so can help shed light on the factors that contribute to racial differences in financial outcomes and instruct us on how to design more efficient and equitable policies.

Authors:

Diana Farrell: JPMorgan Chase Institute, President & CEO

Fiona Greig: JPMorgan Chase Institute, Director of Consumer Research

Chris Wheat: JPMorgan Chase Institute, Director of Business Research

Max Liebeskind: JPMorgan Chase Institute, Research Associate

Peter Ganong: Assistant Professor at the University of Chicago Harris School of Public Policy

Damon Jones: Associate Professor at the University of Chicago Harris School of Public Policy

JPMorgan Chase & Co.'s website terms, privacy and security policies don't apply to the site or app you're about to visit. Please review its website terms, privacy and security policies to see how they apply to you. JPMorgan Chase & Co. isn't responsible for (and doesn't provide) any products, services or content at this third-party site or app, except for products and services that explicitly carry the JPMorgan Chase & Co.