We no longer support this browser. Using a supported browser will provide a better experience.

Please update your browser.

Small businesses, defined as businesses with fewer than 500 employees, play a critical role in the US economy. They provide work for nearly half of all employees in the US and are credited with creating 52 percent of net job growth. Small businesses also account for a significant share of personal income, given their average annual payroll of $45,000 per employee. Despite its importance, relatively little is known about the underlying dynamics of employment growth and volatility at the individual small business level. In particular, publicly available aggregate data provide an incomplete view of the ways in which employment in the sector shapes the financial well-being of small business owners and their employees.

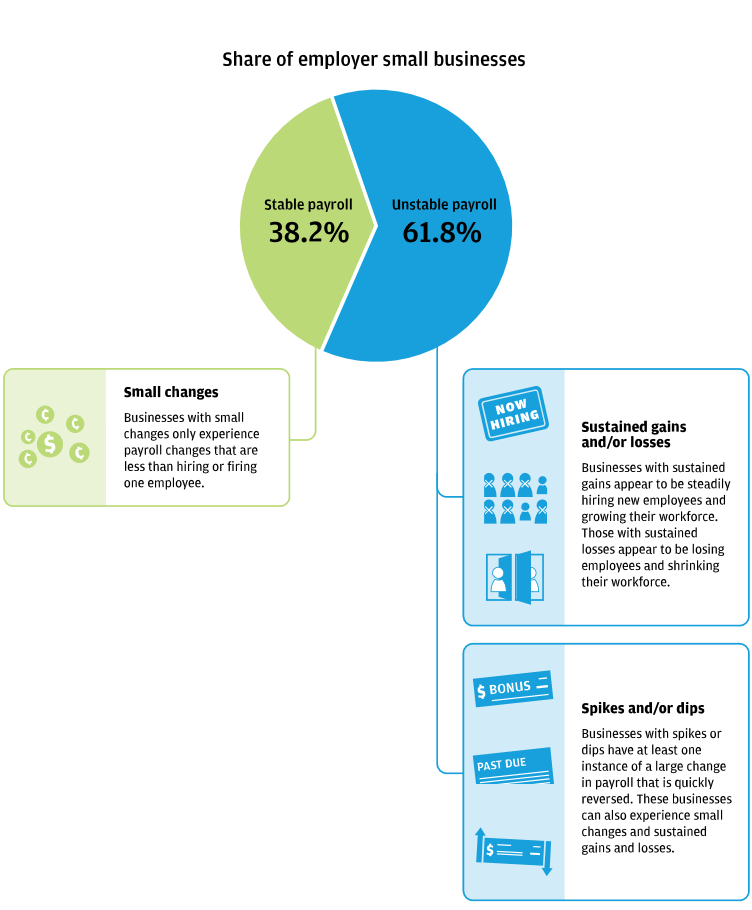

As part of its broader research agenda on the small business sector, the JPMorgan Chase Institute analyzed the size, growth, and volatility of payroll outflows for small businesses. Using a sample of over 45,000 small business customers, we found that payroll is a high expense for most employer small businesses. Furthermore, even though most small businesses experience low payroll growth each year, the month-to-month volatility of payroll expenses around that growth can be quite high, making it more difficult for small business owners to manage their cash flows.

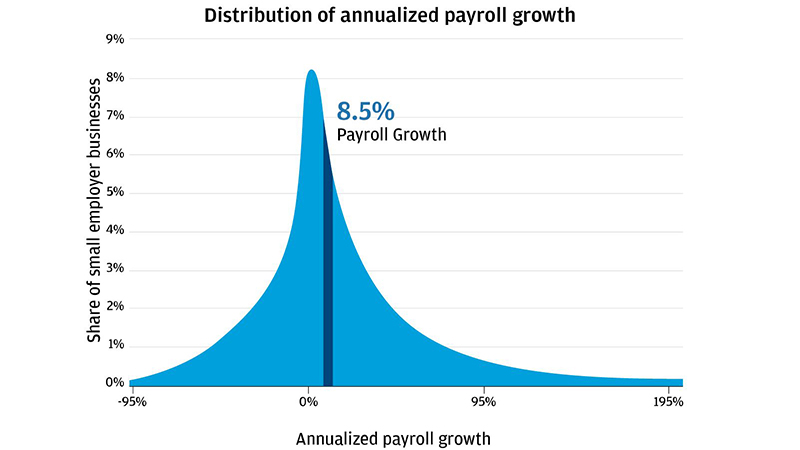

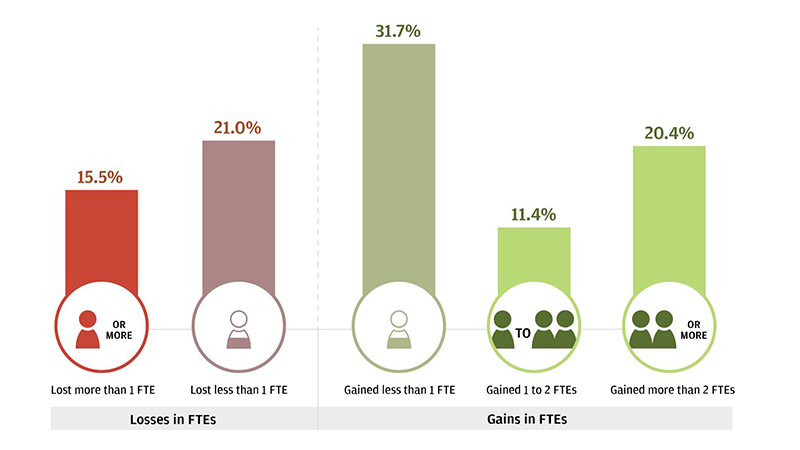

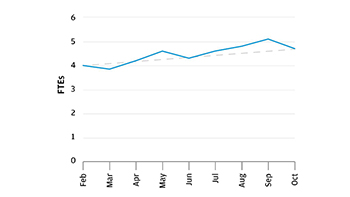

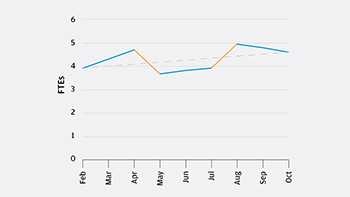

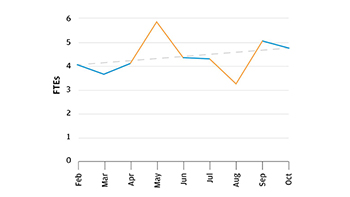

Monthly payroll payments from the median small employer business in our sample grew at an annualized rate of 8.5 percent per year. This growth rate corresponded to the addition of less than one full-time equivalent (FTE). Moreover, 36.5 percent of these firms experienced declining payroll outflows, consistent with the loss of at least a partial FTE. In contrast, 31.8 percent of small businesses experienced growth in payroll outflows consistent with the addition of one or more FTEs.

Note: We calculated annual full-time equivalent (FTE) wages for a firm by dividing the total annual payroll for its 6-digit NAICS industry by the total number of employees in that industry. We identify FTE changes by comparing annualized payroll growth to this annual FTE wage measure. Annual payroll and employee data are from the U.S. Census Statistics of U.S. Businesses.

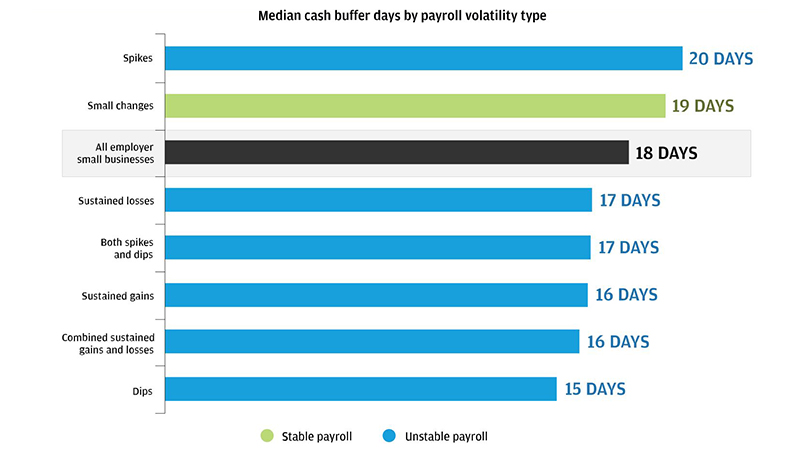

The typical employer small business had payroll outflows of $18,700, or 18 percent of all outflows.

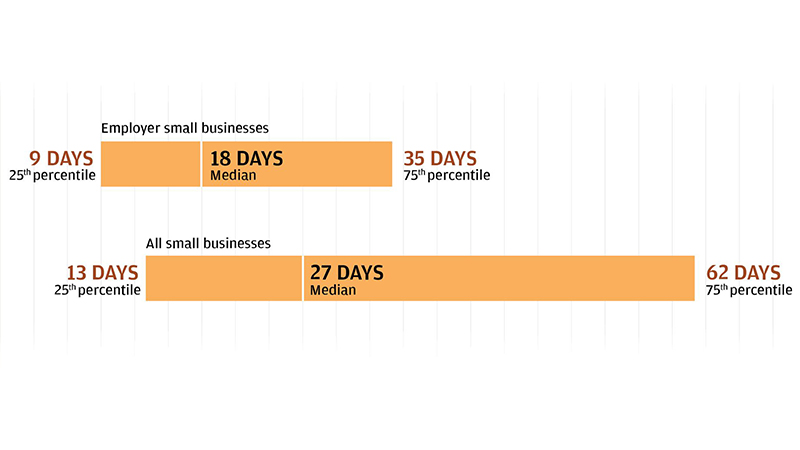

Large payroll outflows can pose significant challenges to small businesses with limited liquidity. We found that across employers and nonemployers, the typical small business only carried 27 cash buffer days. Moreover, the typical employer small business had only 18 cash buffer days, significantly fewer than 27. The size and volatility of payroll expenses may put substantial stress on the relatively limited cash reserves of these employer small businesses.

Cash buffer days are the number of days of cash outflows a business could pay out of its cash balance if its inflows were to stop. We estimate cash buffer days for a business by computing the ratio of its average daily cash balances to its average daily cash outflows.

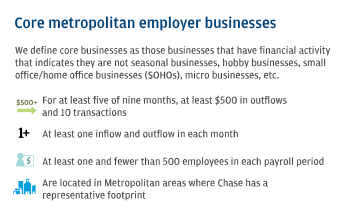

We created a sample of 45,260 small businesses who hold Chase Business Banking deposit accounts and meet our criteria for small, core metropolitan employer businesses. We then used their combined 65 million transactions to produce a view of daily cash inflows, payroll and other cash outflows, and end-of-day balances over the nine non-holiday months from February 2015 to October 2015.

The findings in this report are relevant for policy makers, advocates, and private-sector partners alike. These findings suggest that those who seek to help small businesses should focus not only on new business creation but specifically on minimizing payroll volatility, which can benefit both small business owners and employees. Moreover, they shed light on trade-offs inherent in policies that improve wages of small business employees but impose costs on small business owners.

JPMorgan Chase & Co.'s website terms, privacy and security policies don't apply to the site or app you're about to visit. Please review its website terms, privacy and security policies to see how they apply to you. JPMorgan Chase & Co. isn't responsible for (and doesn't provide) any products, services or content at this third-party site or app, except for products and services that explicitly carry the JPMorgan Chase & Co.