We no longer support this browser. Using a supported browser will provide a better experience.

Please update your browser.

When a natural disaster strikes, the lives of thousands of families are affected. In 2017, the hurricane season in the US drew worldwide attention after hurricanes Harvey, Irma, and Maria struck Houston, Miami, and Puerto Rico, respectively, destroying infrastructure, disrupting the lives of residents, and displacing many households. Widely cited claims about the effects of Hurricanes Katrina and Sandy on small businesses in recent years have drawn increased attention to the impact of these natural disasters on the small businesses in these communities.

Despite this attention, conflicting views persist about the effect of disasters on small businesses. Prior research illustrates the economic and material impact of disasters on small businesses. After Hurricane Sandy, some estimates suggested that between 25 and 40 percent of small businesses impacted by a similar disaster would fail shortly thereafter,1 an exit rate meaningfully higher than the 10 percent annual rate for employer small businesses observed nationwide that same year.2 Such failure rates suggest that hurricanes and other natural disasters have a pronounced economic impact on those firms actually affected by a natural disaster. Moreover, hurricanes may affect a nontrivial fraction of small businesses in an affected area. For example, Hurricane Sandy was estimated to have negatively impacted between 60,000 and 100,000 small businesses.3 This reflects 5 percent of all small businesses in the New York metro area, and up to 25 percent of all employer small businesses in the area.4

Key Facts

In contrast, recent administrative data suggest a more muted and short-lived financial impact of Harvey and Irma on small businesses. Specifically, a recent study of credit card purchases suggested that Harvey and Irma had a dramatic but short-term impact on total small business revenues. This study found that small business average daily revenue fell to 7 to 13 percent of prior levels, but grew to normal levels in about a week.

In short, while disasters may have a substantial economic and material impact on small businesses, the financial resiliency of these businesses in the face of a disaster is less clear. The extent to which a large if short-term drop in revenues impacts the overall financial health of a small business depends critically on the timing and extent of changes in its expenses and other cash flows. Moreover, analyses of small business financial outcomes segmented by industry and zip code can provide policy makers with additional insight about which small businesses were affected.

This report aims to fill this gap by drawing from JPMorgan Chase Institute data to assess the impact of hurricanes Harvey and Irma on small business inflows, outflows, and balances through November 2017.5 To this end, we focus on an anonymized sample of over 40,000 firms, whose owners resided in the same zip code in Houston and Miami metro areas since July 2016 and showed sufficient financial activity since the beginning of 2015, in addition to meeting other basic sampling criteria.6

We find that cash flows retracted significantly: inflows in the week after landfall declined by 63 percent year-over-year for the typical firm in Houston and 82 percent in Miami, only partially mitigated by a 54 percent median drop in outflows in Houston and one of 62 percent in Miami, resulting in a drop in balances of nearly 8 percent. We further find that small construction businesses and small repair and maintenance firms had the strongest balance growth after Harvey and Irma, and that few small businesses across most neighborhoods across Houston and Miami saw depressed revenues for more than four weeks after landfall. While these hurricanes may well have longer-term material and economic impacts on the sector in Houston and Miami, our analyses suggest that, at least in the short-run, many small businesses showed a surprising degree of financial resiliency.

Cash balances provide a useful view of the financial well-being of many small businesses. Most small businesses face meaningful cash liquidity constraints especially given the challenges many face in quickly attaining access to external capital.7 While these small businesses may not be able to quickly manage their cash reserves through external finance, they may be able to cushion the impact of significant shortfalls in revenues or other cash inflows by managing their short-term expenses and other payments. To that end, we first describe the impact of Harvey and Irma on small business cash account balances in the Houston and Miami metro areas. We then explore how changes in cash inflows and outflows drove these observed changes in balances.

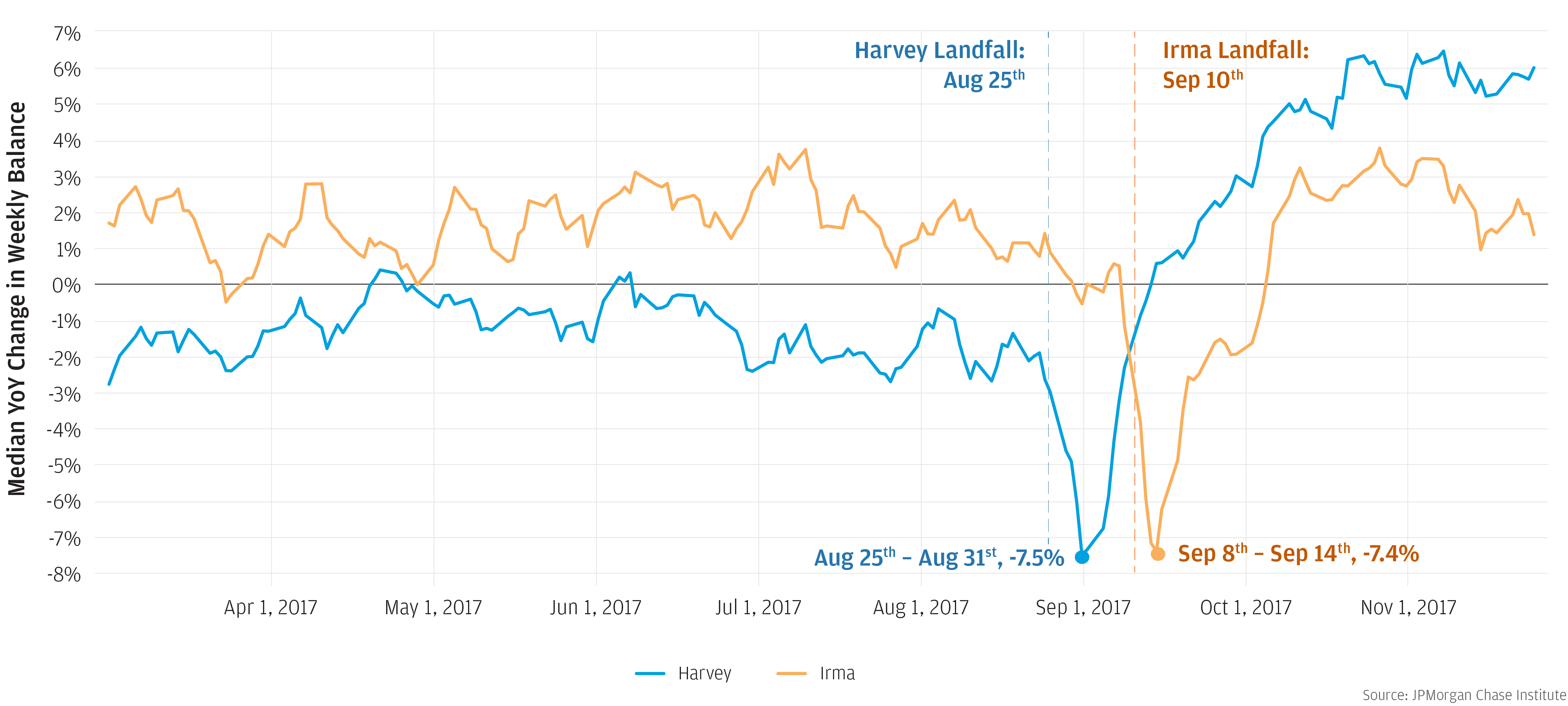

Cash balances declined by at least 7.4 percent for most small businesses in Houston and Miami after Harvey and Irma, but recovered within two to three weeks

In order to assess the impact of Harvey and Irma on cash liquidity, we compared the average weekly balance for a given firm to its average balance for the week 52 weeks prior. Figure 1 shows the progression of the median of this year-over-year (YoY) measure8 for small businesses in Houston and Miami. In both cities, the median decline in cash balances for small businesses was nearly eight percent in the weeks following Harvey and Irma. In Houston, most small businesses had cash balance declines of at least 7.5 percent by August 31st, while cash balances declined for most small businesses by 7.4 percent in Miami by September 14th. Notably, cash balances for the typical business in Miami were growing faster than balances for the typical business in Houston in the first half of 2017, suggesting that the relative impact of Irma on cash liquidity in Miami may have been larger than the impact of Harvey in Houston.

However, this cash balance view suggests that most small firms in both cities showed a meaningful level of financial resiliency in the face of these storms. In both cities, cash balances recovered for most firms within two to three weeks. Most small businesses in the Houston metro area had cash balances at least as high as they were one year prior by September 14th, and most small business cash balances in the Miami metro area recovered to this level by October 5th. Beyond this recovery, most small business owners continued to increase the cash held in their deposit accounts through the end of our observation window.

To better understand how these small businesses achieved this financial resiliency, we turn to changes in cash inflows and outflows. Views of consumer spending by Houston and Miami residents and card spending at small customer-facing businesses in Houston and Miami, both from Chase and other card vendors, collectively suggest that spending at consumer-facing businesses of all sizes dropped significantly after Harvey and Irma. Our view of inflows into both business-to-business and business-to-consumer businesses shows a similar pattern.

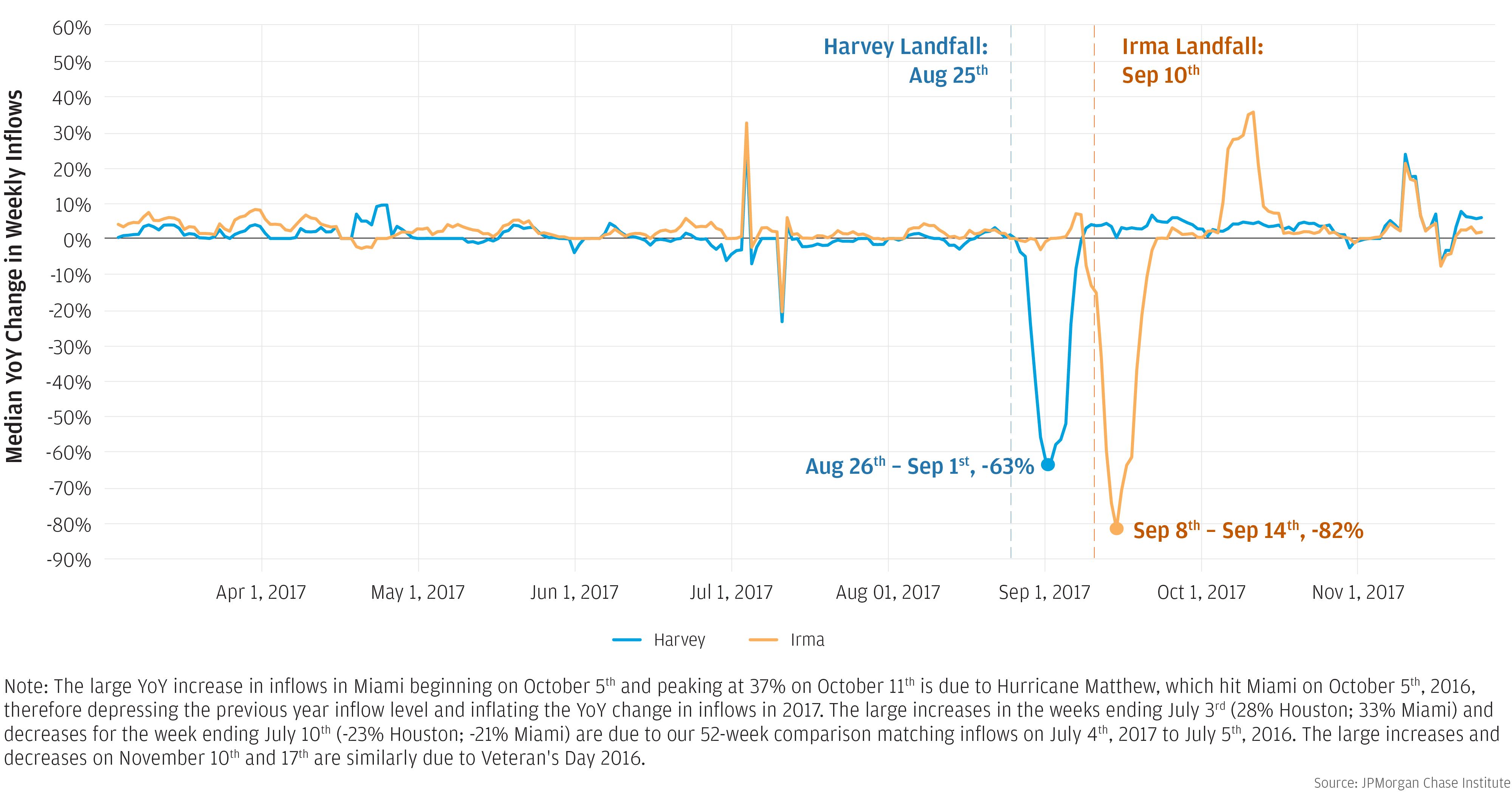

Figure 2 shows dramatic declines in revenues and other cash inflows in the days after Harvey and Irma. In the Houston metro area, inflows reached their trough on the week ending on September 1st, when most of the firms in our sample received inflows at least 63 percent lower than they had the year prior, and 31 percent received no inflows at all for the week. The financial impact of Irma in Miami was even larger. During the week ending September 14th, most firms in the Miami metro area received inflows at least 82 percent lower than the week one year prior, and 41 percent had no inflows at all. These declines were sizable—the median firm typically saw year-over-year changes in inflows of a few percentage points in either direction for most days in 2017 leading up to these events. Also, only 13 percent of firms in Houston and 17 percent of firms in Miami experienced no inflows in these same weeks the year before.

While the decline in inflows was sharp after the landfall of Harvey and Irma, inflows returned to positive year-over-year growth in about a week in both Houston and Miami. The majority of small businesses in the Houston metro area returned to positive year-on-year inflow growth by September 8th, one week after the lowest point. Along similar lines, the majority of small businesses in the Miami metro area achieved positive inflow growth by September 22nd, eight days after the trough.

Cash inflows dropped by over 63 percent for most small businesses, and inflows for most recovered in about a week

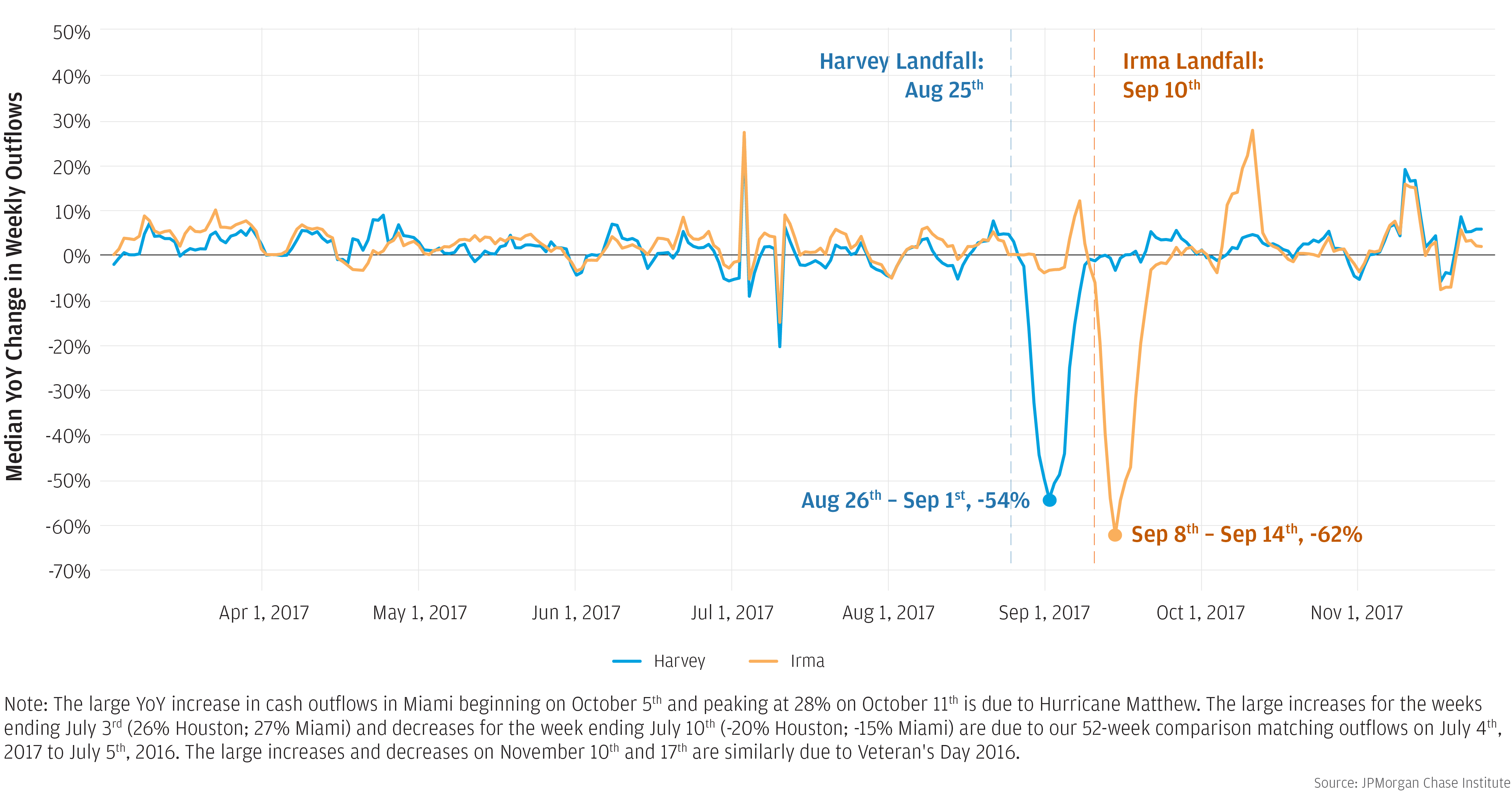

All else equal, a small business experiencing a large drop in inflows might see a permanent drop in cash balances, even if the drop in inflows only lasted for a week. However, the data show that balances recovered and even grew in the short run for most small businesses. In fact, our data suggest that many small businesses responded to depressed revenues and other inflows by pulling back expenses and other outflows. Figure 3 shows that the typical firm in the Houston metro area saw its biggest reduction in outflows during the week leading up to September 1st, when outflows were 54 percent lower than they were 52 weeks prior. The typical firm in the Miami metro area saw its largest reduction during the week leading up to September 14th, with outflows down by 62 percent year-over-year. As with inflows, small businesses in both Houston and Miami typically experienced relatively small year-over-year changes in outflows earlier in 2017.

Cash outflows dropped by over 54 percent for most small businesses, and outflows for most recovered in two to three weeks

While the decline in outflows was smaller in magnitude than the decline in inflows at their respective troughs, the decline in outflows lasted about a week longer than the decline in inflows. In Houston, by September 18th, most firms showed positive year-over-year growth in outflows, 17 days after the lowest point we observed. In Miami, while outflows recovered less quickly than inflows, they recovered faster than in Houston, with most firms showing positive year-over-year growth in outflows by September 26th—12 days after their lowest point.

Taken together, these views of balances, inflows and outflows show that most small businesses in the Houston and Miami metro areas showed considerable financial resiliency in response to Hurricanes Harvey and Irma. Most small businesses saw large reductions in inflows matched by drops in outflows of a slightly smaller magnitude. The initial drop in inflows caused cash balances to also drop for most firms, though less than they would have if outflows had not also retracted by a similar magnitude. The typical firm then saw a recovery in inflows in about a week, but a somewhat slower recovery of outflows within two to three weeks. This caused cash balances to recover to their prior growth rates, and most firms saw year-over-year increases in their cash balances.

While major hurricanes like Harvey and Irma substantially disrupt businesses, the extent of disruption and the response of small businesses can vary meaningfully by industry. To better understand these differences in financial impact, we analyzed balances, inflows, and outflows by industry in the week after landfall and over time.

Small businesses experienced large financial impacts across most industries in the week just after landfall

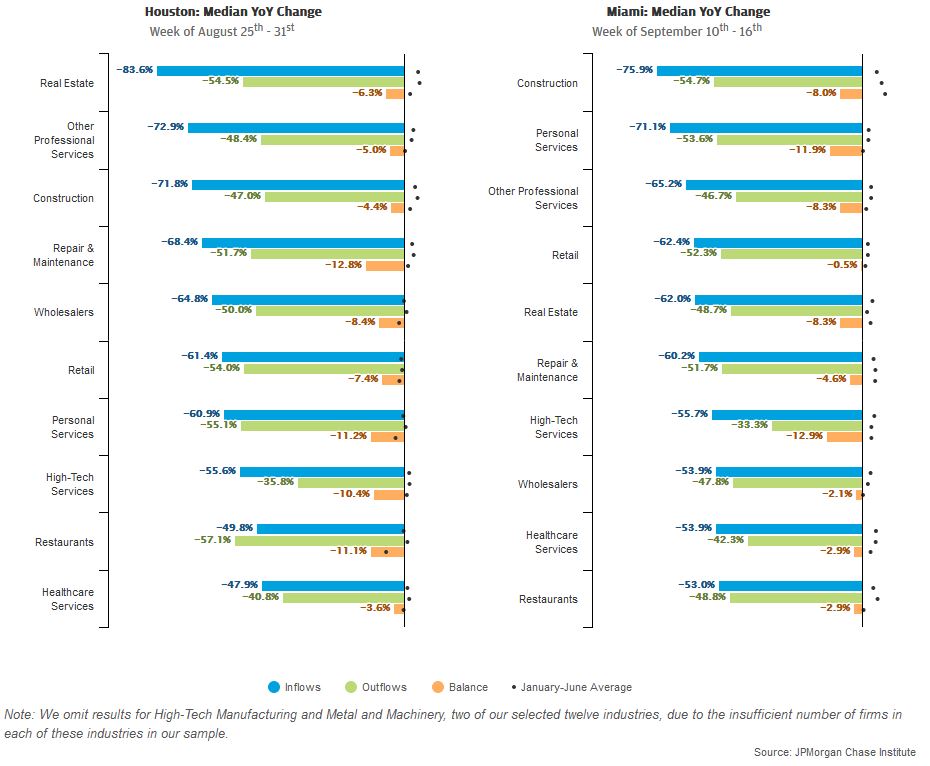

In both Houston and Miami, cash flows and balances declined across industries in the week following Harvey and Irma, as shown in Figure 4. For each of ten industries, the figure shows median year-over-year changes in balances, inflows, and outflows in the week following Harvey and Irma, and compares these to average weekly year-over-year changes in balances, inflows, and outflows for the first six months of 2017. While small businesses across all industries sustained large financial impacts in the days following Harvey and Irma, some short-term differences stand out. In the week after Harvey, small real estate firms in Houston saw the largest impact in inflows, with inflows declining at least 84 percent year-over year. In contrast, inflows to small healthcare service providers in Houston were least affected, where most businesses saw year-over-year decreases in inflows of 48 percent or less, and decreases in outflows of 41 percent or less. In the week following Irma, Miami small construction firms experienced the largest year-over-year declines in both inflows and outflows—during that week, inflows to small Miami construction firms were at least 76 percent lower year-over-year, and outflows were at least 55 percent lower. Small restaurants in the Miami metro area saw the smallest declines in inflows directly after landfall. Inflows to most small Miami restaurants decreased by 53 percent or less during the week after Irma.

Over the subsequent weeks, even larger differences across industries emerged, particularly with respect to cash balances. Figure 5 depicts median weekly year-over-year changes in cash balances, inflows, and outflows in both the Houston and Miami metro areas, for each of ten industries, from two weeks prior to landfall until the end of our observation window—twelve weeks after landfall in Houston and ten weeks after landfall in Miami. Figure 5 also presents the average median weekly year-over-year change in cash balances, inflows, and outflows for the first six months of 2017 as a point of context and comparison.

Figure 5: Small businesses experienced large financial impacts across most industries, with subsequent balance growth in the construction, repair and maintenance industries

Median YoY Change in Weekly Balances

Median YoY Change in Weekly Inflows

Median YoY Change in Weekly Outflows

Note: The large YoY increase in cash inflows and outflows in Miami during the third week after Irma landfall is due to Hurricane Matthew, which reached Miami during the first week of October 2016.

In both the Houston and Miami metro areas, small construction businesses and small repair and maintenance businesses appear to show the greatest financial resiliency in the first weeks after Harvey and Irma. Twelve weeks after landfall, most small construction businesses in Houston had cash balances at least 20 percent higher and inflows at least 25 percent higher, and most small repair and maintenance businesses had balances at least 9 percent higher and inflows at least 4 percent higher year-over-year. Along similar lines, ten weeks after landfall, cash balances at most small construction businesses in Miami were up at least 7 percent and inflows were up at least 6 percent, and most small repair and maintenance businesses had balances at least 9 percent higher and inflows at least 3 percent higher. In contrast, in both Houston and Miami, small healthcare services, real estate, and high-tech services businesses were among the slowest to see balance growth recovery.

Our first finding characterizes the extent of economic impact across the Houston and Miami metro areas overall. Our data also allow us to explore the financial impact of Harvey and Irma on individual neighborhoods. We explore this by identifying the share of small businesses in individual zip codes that experienced year-over-year weekly inflow losses greater than 50 percent. Figures 6 and 7 show the progression of this measure of impact from four weeks before the Hurricanes Harvey and Irma made landfall until twelve and ten weeks afterwards, respectively.

Note: For each zip code, this map displays the share of firms that had year-over-year inflow losses greater than 50 percent in the seven-day period leading up to and including the day indicated by the slider. Zip codes that have grey hash lines have been censored because they did not clear our reporting threshold for number of firms.

Source: JPMorgan Chase Institute

In both Houston and Miami, there was meaningful variation across neighborhoods in the week directly after landfall, but four weeks after Hurricanes Harvey and Irma struck, neighborhoods in both metro areas appeared to have a similar concentration of severely impacted firms than they did before landfall. During the week after landfall in Houston, small businesses in the 77026 zip code (Kashmere Gardens) were the most likely to see large declines in inflows, where 72 percent of small businesses saw declines of 50 percent or more year-over-year. In contrast, only 44 percent of small businesses in the 77382 zip code (Sterling Ridge-Alden Bridge) saw similarly large declines in inflows, the lowest share among the zip codes we analyzed in the Houston metro area. However, by four weeks after landfall, the share of businesses with declining inflows in these two neighborhoods returned to their pre-hurricane levels. Four weeks out, 18 percent of small businesses had significant inflow declines in the 77026 zip code, and 21 percent had significant inflow declines in the 77382 zip code. These levels, while high, are similar to the levels observed four weeks prior to Harvey, when 26 percent of small businesses in the 77026 zip code and 25 percent of the small businesses in the 77382 zip code saw declines in inflows over 50 percent.

Note: For each zip code, this map displays the share of firms that had year-over-year inflow losses greater than 50 percent in the seven-day period leading up to and including the day indicated by the slider. Zip codes that have grey hash lines have been censored because they did not clear our reporting threshold for number of firms.

Source: JPMorgan Chase Institute

Neighborhoods in the Miami metro area showed a similar pattern—in the week after Irma, 74 percent of small businesses in the 33133 zip code (Coconut Grove) had inflows at least 50 percent lower than they did the prior year, more than any other zip code in the Miami metro. That same week, only 32 percent of small businesses in the 33066 zip code (Coconut Creek) were similarly impacted. Four weeks after landfall, 29 percent of small businesses still had inflows down by at least 50 percent year-over-year in both of these zip codes. As was the case in Houston, these levels were quite similar to levels observed four weeks before the storm, when 28 percent of small businesses in both zip codes had significantly reduced inflows year-over-year.

Our findings suggest that while there was a significant if short-term financial impact to small businesses and the families that own them in the face of Harvey and Irma, many small business owners showed a marked resilience in the face of these impacts. At least in the short-run, balances and balance growth returned to normal levels for the typical firm after a period of depressed activity and curtailed inflows and outflows.

While most small business balances appear to have financially recovered within a few weeks after landfall, the large reductions in inflows and outflows experienced by most small businesses were material and significant for the Houston and Miami economies. They correspond to several days of missed economic activity and suggest a meaningful loss to small business suppliers and customers. This also suggests a substantial welfare loss to both small business customers who were unable to secure goods and services, and to small business suppliers who experienced a gap in their sales.

However, while we observe a relatively quick short-term recovery in cash balances, many small businesses may have experienced losses in physical assets unobserved by our data. If it is the case that small business owners are holding back on necessary expenses related to repairing damaged fixed assets, it is important to track whether the resilience of small businesses in Houston and Miami persists and to identify policies that could potentially strengthen the finances of these businesses. With a complete, data-driven picture of recovery, policy makers can ensure recovery outlasts not only this, but also future hurricane seasons.

We especially thank our research analyst, Beatriz Rache for her hard work generating analytics and contributing to the production of this report.

This effort would not have been possible without the critical support of the JPMorgan Chase Intelligent Solutions team of data experts, including Brent Warshaw, Gaby Marano, Stella Ng, Michael Harasimowicz, and Bill Bowlsbey, and JPMorgan Chase Institute team members including Chenxi Yu, Carlos Grandet, Caitlin Legacki, Courtney Hacker, Gena Stern, Natalie Holmes, Alyssa Flaschner, Jolie Spiegelman, and Kelly Benoit.

We would like to acknowledge Jamie Dimon, CEO of JPMorgan Chase & Co., for his vision and leadership in establishing the Institute and enabling the ongoing research agenda. Along with support from across the firm—notably from Peter Scher, Len Laufer, Max Neukirchen, Patrik Ringstroem, Joyce Chang, and Judy Miller—the Institute has had the resources and support to pioneer a new approach to contribute to global economic analysis and insight.

Farrell, Diana and Christopher Wheat. 2018. “Bend, Don’t Break: Small Business Financial Resilience After Hurricanes Harvey and Irma.” JPMorgan Chase Institute.

JPMorgan Chase & Co.'s website terms, privacy and security policies don't apply to the site or app you're about to visit. Please review its website terms, privacy and security policies to see how they apply to you. JPMorgan Chase & Co. isn't responsible for (and doesn't provide) any products, services or content at this third-party site or app, except for products and services that explicitly carry the JPMorgan Chase & Co.