We no longer support this browser. Using a supported browser will provide a better experience.

Please update your browser.

The growth of the Online Platform Economy (OPE) has been contributing to the changing nature of work. Is this marketplace building momentum towards systemic change in the labor force, or will it remain a small market for supplementary income? In previous work we highlighted that growth in participation on labor and capital platforms has peaked. As of June 2016, participation on labor platforms has doubled year-over-year, but participation on capital platforms has leveled off. In this report, we explore the dynamics of participation and earnings in order to better understand how growth has slowed. We draw from one of the largest samples of platform participants to date: over 240,000 anonymized individuals who have received platform income between October 2012 and June 2016 from one or more of 42 different platforms. Our findings point to several dimensions of how the growth in online platform participation has slowed.

In sum, growth in online platform participation is highly dependent on attracting new participants or increasing engagement of existing participants. As outside options improve, recruiting and retaining platform workers might become increasingly difficult and could constrain future growth.

The growth of the Online Platform Economy (OPE) has been contributing to the changing nature of work. With more than four percent of adults earning income by selling goods or services through platforms that connect them directly to customers, and many more participating in other forms of contingent work, the labor market now offers more easily accessible opportunities to earn income. Others have documented the recent growth, and continued growth potential, of independent work more broadly as well as by platforms specifically. 1 Is this marketplace in fact building momentum towards systemic change in the labor force, or will it remain a fringe market for supplementary income?

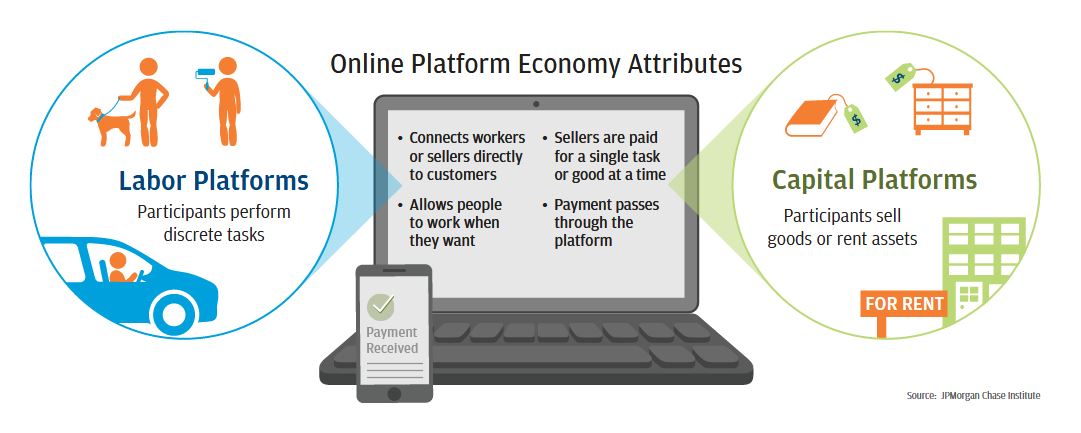

In previous work we highlighted that although participation in labor and capital platforms continues to grow quickly, the growth rates have peaked (JPMorgan Chase Institute, 2016a). Here we explore the dynamics of participation and earnings in order to better understand how growth has slowed. Building on our initial OPE data asset released in our February 2016 report Paychecks, Paydays, and the Online Platform Economy , we report on one of the largest samples of platform participants to date: over 240,000 anonymized individuals who have received income at least once between October 2012 and June 2016 from at least one of 42 different platforms (Farrell and Greig, 2016). 2 We distinguish between labor platforms and capital platforms (Figure 1). Labor platforms, such as Uber or TaskRabbit, and which are sometimes referred to as the “gig economy,” connect customers with freelance or contingent workers who perform discrete tasks or projects. Capital platforms, such as Airbnb or eBay, connect customers with individuals who lease assets or sell goods peer-to-peer. 3

Our findings point to several dimensions of how the growth in participation on online platforms has slowed. First, we document that the rate of growth in participation in the Online Platform Economy peaked in 2014 and has slowed since then. Second, monthly earnings from labor platforms have fallen since June 2014, a trend that coincides with wage cuts by some platforms. Third, turnover among the online platform workforce is high: one in six participants in any given month is new and more than half of participants exit within 12 months. Fourth, turnover is particularly high among employed, higher-income, and younger participants. Finally, as the labor market has strengthened, the share of participants with outside employment, a segment that exhibits lower attachment to platform work, has increased on both labor and capital platforms. In sum, growth in online platform participation is highly dependent on attracting new participants or increasing attachment of existing participants. As outside options improve, recruiting and retaining platform workers might become increasingly difficult.

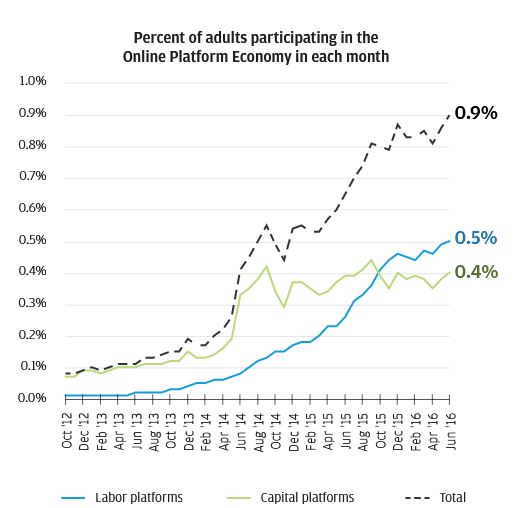

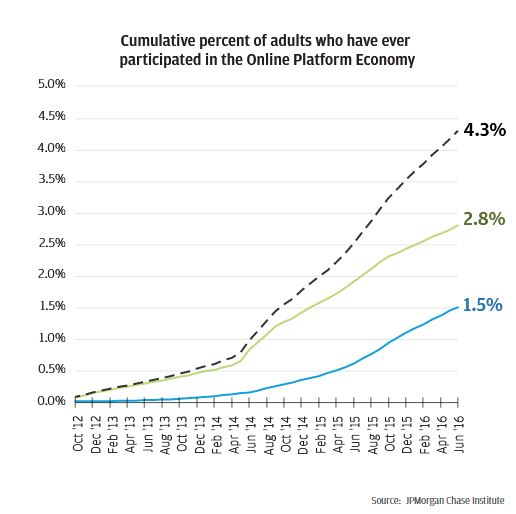

Participation in the Online Platform Economy continued to grow through 2015 and the first half of 2016, but that growth slowed compared to earlier periods. In June 2016, 0.9 percent of adults actively earned income from the Online Platform Economy, including 0.5 percent from labor platforms and 0.4 percent from capital platforms (Figure 2). Cumulatively, 4.3 percent of adults earned income from the platform economy over this timeframe—1.5 percent from labor platforms and 2.8 percent from capital platforms.

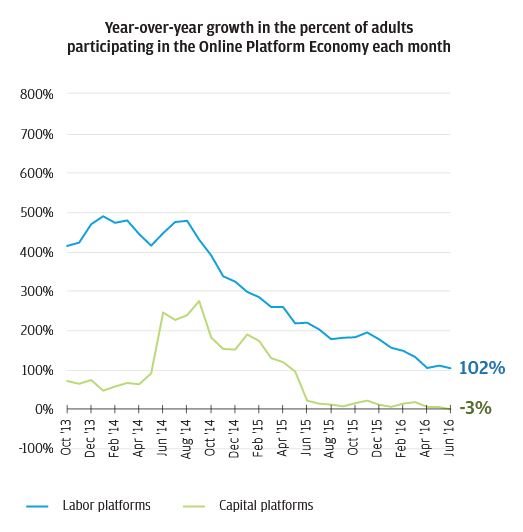

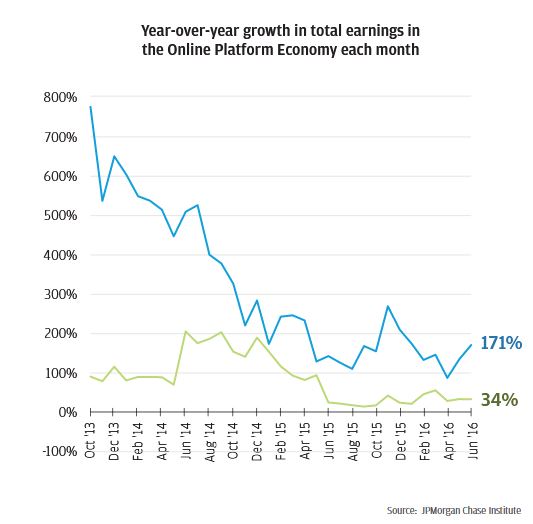

Starting in late 2015 and continuing into the first half of 2016, monthly participation on capital platforms leveled off (Figure 2). Monthly participation on labor platforms continued to grow, albeit at a much lower rate in 2016 compared to prior years. As of June 2016, participation in capital platforms exhibited no year-over-year growth, but participation in labor platforms doubled year-over- year (Figure 3). 4 While growth in participation has slowed, the share of participants earning income from multiple platforms has increased but remains small. As of June 2016, 18 percent of participants earned income from multiple labor platforms, 3 percent of participants earned income from multiple capital platforms, and 1 percent of participants earned income from both types of platforms (see Figure 16 in the Appendix for the full time series of these shares). Year-over-year growth in platform earnings also slowed from over 200 percent for both labor and capital platforms in 2014 to 171 percent on labor platforms and 34 percent on capital platforms as of June 2016 (Figure 3).

Thus, while growth rates in participation and platform earnings have slowed, they remain relatively flat for capital platforms. This is consistent with speculation by others that the near-term growth potential for independent work might be higher for online labor platforms compared to online capital platforms. For example, Manyika et al. (2016) estimated that the number of independent workers providing labor services is more than five times larger than the number of independent workers selling goods or renting assets: around 150 million and 8 million across the US and Europe, respectively. 5 However, the share of independent worker income earned through online platforms is much lower for labor services (6 percent) compared to selling goods (63 percent) or leasing assets (36 percent). As we show below, high turnover and an improving traditional labor market are a few factors that might hinder that growth in the Online Platform Economy going forward.

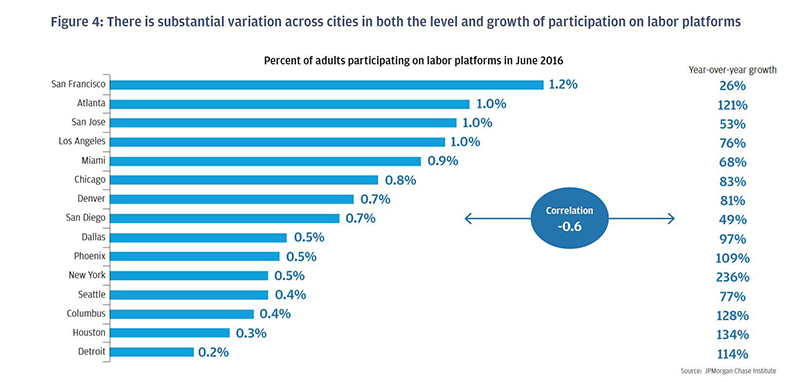

At the city level, there is substantial variation across cities in both the level and growth of labor platform participation. In June 2016, participation on labor platforms ranged from 1.2 percent of adults in San Francisco to 0.2 percent in Detroit (Figure 4). New York experienced the fastest growth in participation—a 236 percent increase year-over-year—while San Francisco experienced the slowest rate of growth at 26 percent year-over-year. In general, cities with lower participation rates grew faster than cities with higher participation rates: there is a cross-city correlation of -0.6 between labor platform participation levels in June 2016 and year-over-year growth between June 2015 and 2016. This implies that labor platform participation is converging across cities, as cities with lower levels of participation “catch up” to cities that already have higher participation rates. A number of city-specific factors, however, likely influence this relationship and the future trajectory of participation, including differences in regulations and demand for platform services.

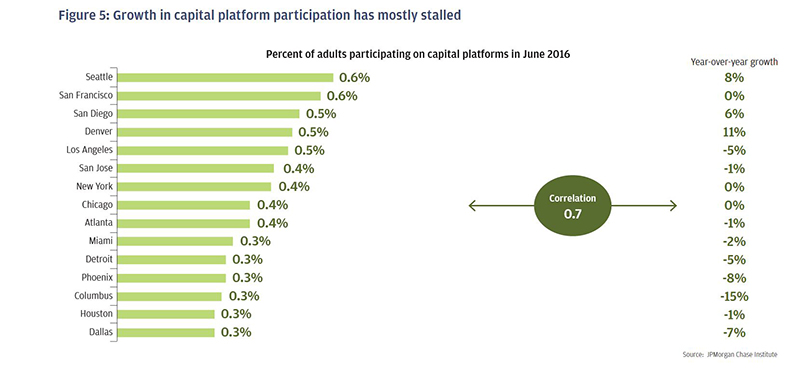

Across the 15 cities there was considerably less variation in participation on capital platforms, and participation growth was relatively flat. Participation rates range from 0.6 percent of adults in Seattle to 0.3 percent in Dallas (Figure 5). Growth in participation was virtually flat in most cities, with Denver experiencing the most year-over-year growth (11 percent) and Columbus experiencing the least (-15 percent). The cross-city correlation between participation levels and growth was 0.7 in June 2016, in contrast to labor platforms, where participation levels and growth were negatively correlated. In other words, cities with the highest capital platform participation were cities that had continued to experience positive growth in participation. As a result, participation levels are not necessarily converging across cities on capital platforms, as they are on labor platforms.

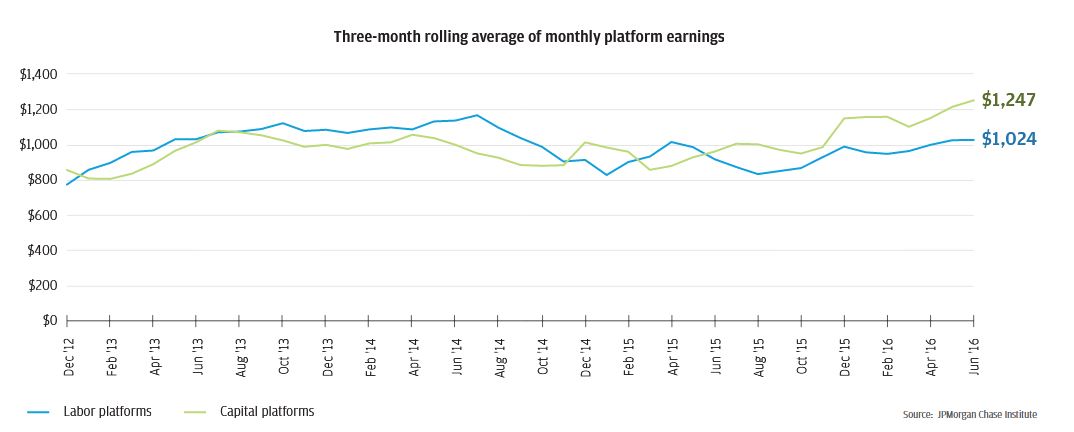

One dimension of the slowing growth in participation is that monthly earnings from labor platforms fell between June 2014 and June 2016. While earnings on both types of platforms grew over the full time period, this overall trend masks a more recent decline in labor platform earnings. The three-month rolling average of nominal monthly earnings on labor platforms grew by 51 percent from December 2012 to June 2014 but fell by 6 percent between June 2014 and June 2016 (Figure 6). 6 On capital platforms, average earnings grew by 11 percent prior to June 2014 and 35 percent between June 2014 and June 2016.

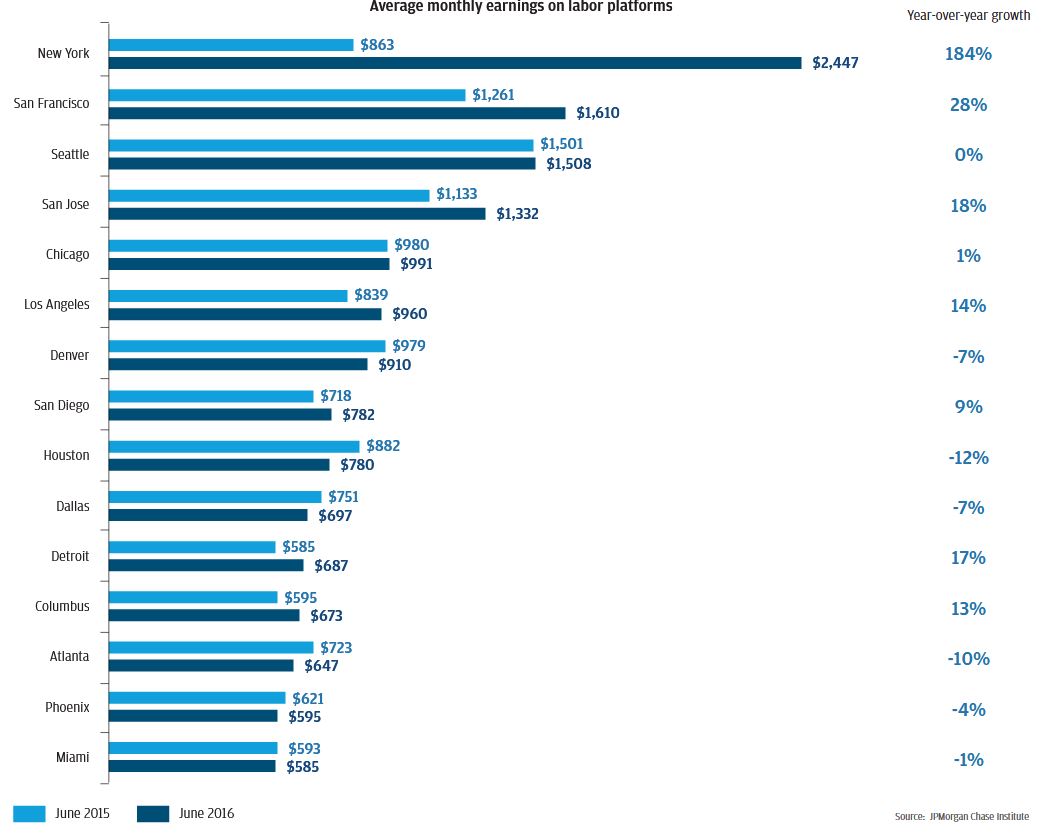

Examining monthly platform earnings within 15 metro areas, we observe that labor platform earnings differ by more than a factor of four across cities (Figure 7). In June 2016, average monthly labor platform earnings ranged from $2,447 in New York to $585 in Miami. Six out of the 15 cities experienced a year-over-year decline in earnings. Nine cities experienced an increase in monthly earnings, ranging from 1 percent growth in Chicago to 184 percent in New York.

What do we make of the fact that earnings from labor platforms have been decreasing in some cities? These lower earnings could be due to a decline in per-task pay or hours worked, or both, though these declines could still be offset by increases in demand and the number of tasks a worker completes while active on the platform. Although we do not observe prices or the quantity of hours worked, some labor platforms reduced the rates they pay participants, the prices they charge customers , or both (Bensinger, 2016; Wang, 2016). 7 These practices have been particularly prevalent on ride-hailing apps, which have increasingly offered cheaper ride- splitting options that compete with public transit. 8 Another motive for platform companies to reduce pay is to cut costs as a way to increase platform profitability, a necessary trend as private equity funding has tightened in 2016 and funding deal terms have become more aggressive (KPMG and CB Insights, 2016; Mims, 2016).

Following these pay cuts, it remains to be seen whether participants will continue to provide the same services, and if new participants will continue to be drawn to platforms for potentially lower pay. Even before the decrease in monthly labor platform earnings, platform work remained a secondary source of income for the majority of participants. 9 Labor platform participants relied on platform income for only 24 percent of their total annual income (Figure 18), and platform earnings offset dips in their non- platform income (Farrell and Greig, 2016).

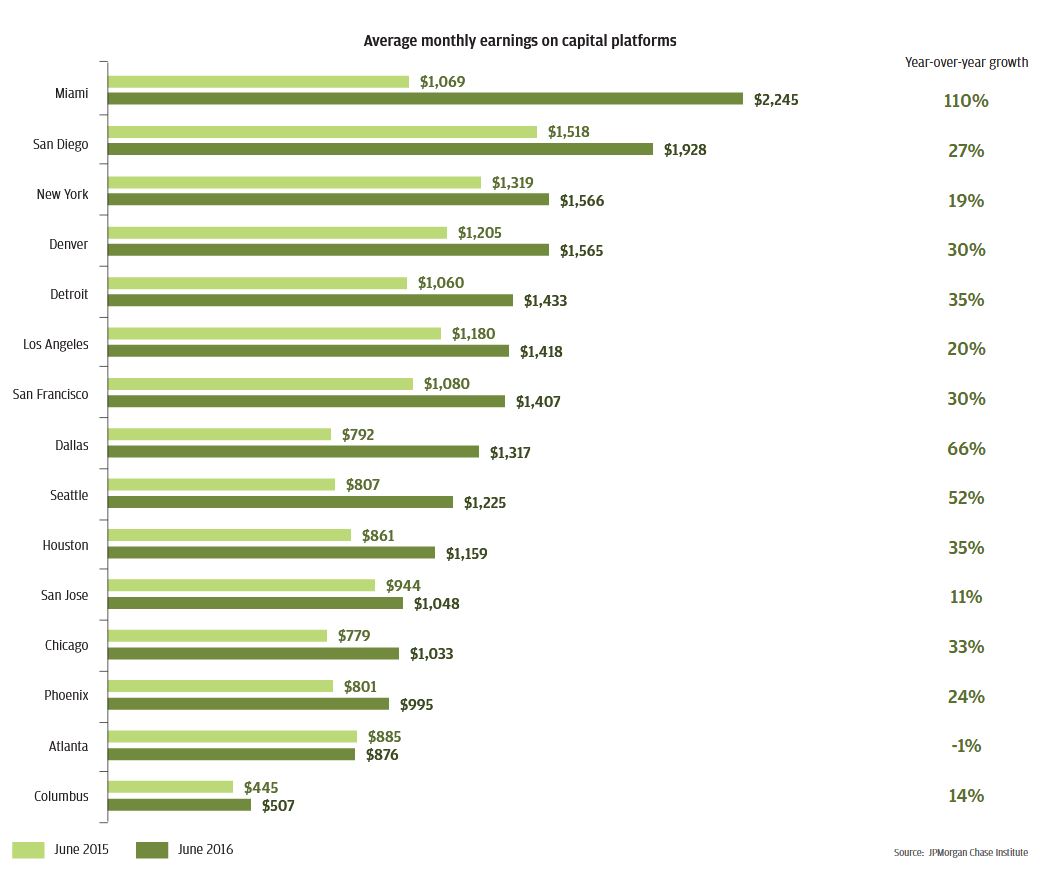

On capital platforms, there was again a four-fold difference in the level of earnings across cities—ranging from $2,245 in Miami to $507 in Columbus (Figure 8). Capital platform earnings increased year-over-year in almost all 15 cities. Participants in Miami experienced more than a doubling in monthly earnings, while earnings growth in Atlanta fell one percent year-over-year.

Capital platform income increased in 2016 across all cities, while participation growth remained flat in most places. This could reflect an increase in online retail spending but not necessarily a commensurate growth in the percent of online retailers who are independent workers. Given that capital platform participants relied on platform income for just 10 percent of their total annual income (see Figure 18) and used it to supplement their non-platform income, platform earnings are more secondary for capital platform participants than labor platform participants (Farrell and Greig, 2016). As a result, their willingness to participate may not be as sensitive to earnings levels as it is for labor platform participants.

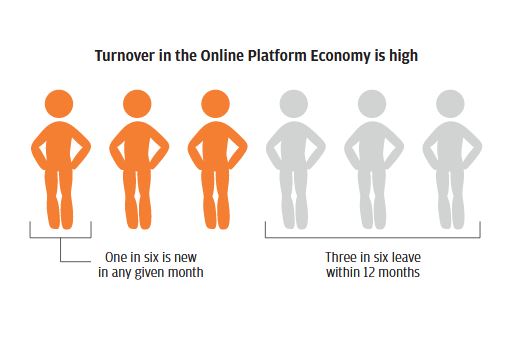

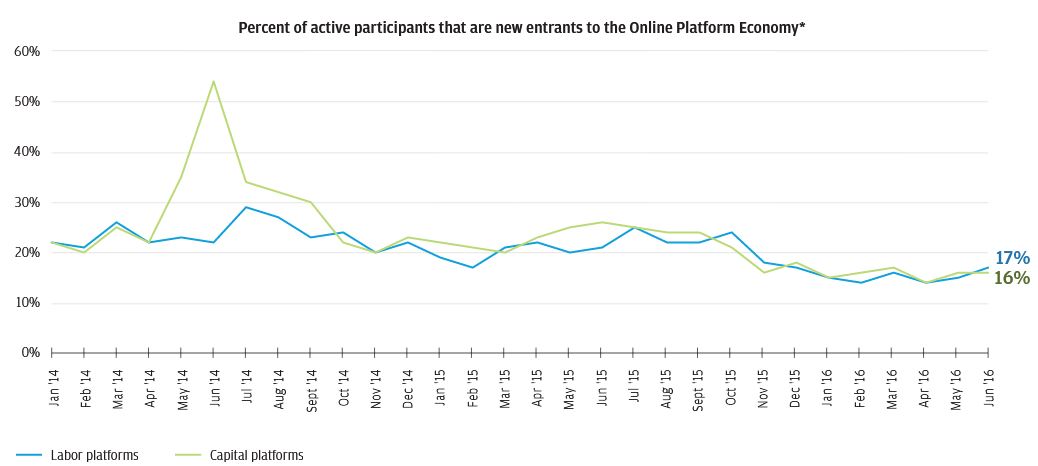

About one in six participants is a new entrant to the Online Platform Economy in any given month across both labor and capital platforms (Figure 9). The share of participants who are newcomers fell from 29 percent for labor platforms in July 2014 and 59 percent for capital platforms in June 2014 to 17 percent on labor platforms and 16 percent on capital platforms in June 2016. 10 Starting in late 2015 and continuing into the first half of 2016, the fraction of active participants who are new entrants decreased slightly, contributing to slower participation growth during the same time period. After the first month of platform participation, though, further participation is quite sporadic. Labor platform participants earned income in only 41 percent of subsequent months, while capital platform participants earned income in just 16 percent of subsequent months. 11

* Data are shown starting in January 2014 because the percentage of participants that are new is mechanically equal to 100% in the first month. Time series are otherwise consistent prior to January 2014. The changing mix of platforms with active participants in any one month resulted in the large spike in new entrants on capital platforms in mid-2014.

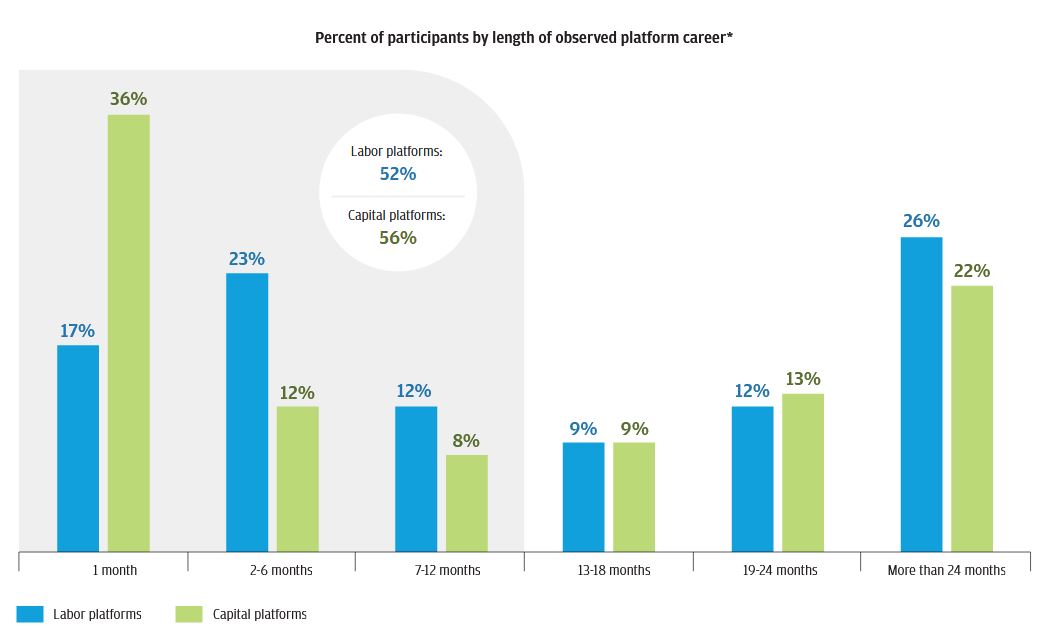

Platform careers are also very short-lived. 12 Slightly more than half of Online Platform Economy participants—52 percent of labor platform participants and 56 percent of capital platform participants—exit the platform economy within 12 months (Figure 10). 13 More than one-third of capital platform participants, meanwhile, earned platform income for just one month compared to 17 percent of labor platform participants.

* Data reflect all participants who first earned platform income in July 2014 or earlier. Platform careers are defined as the number of months between the first month with observed platform income and the last month with observed platform income, without requiring receipt of platform income in the intervening months.

This high degree of turnover suggests that participants might not treat platforms like traditional jobs, where, according to the Bureau of Labor Statistics , the median length of time a wage and salary worker has been with his or her current employer is over four years (Bureau of Labor Statistics, 2016). This might be because platforms as of yet do not typically offer the full package of income security, benefits, training, and income and career progression that many traditional jobs offer. By offering the flexibility to work when and wherever participants want, platforms might have difficulty creating organizational commitment, work-group cohesion, and promotion opportunities—some of the typical predictors of employee retention in traditional jobs. 14 High turnover also implies that growth in online platform participation is highly dependent on attracting new participants or increasing the attachment of existing participants (either by lengthening their careers or increasing the percent of time they are active during their careers). As mentioned above, participants are active less than half of the time during their platform careers (42 percent of months for labor platform participants and 16 percent of months for capital platform participants). If the fraction of active participants who are new entrants continues to decline, then growth in participation could continue to slow.

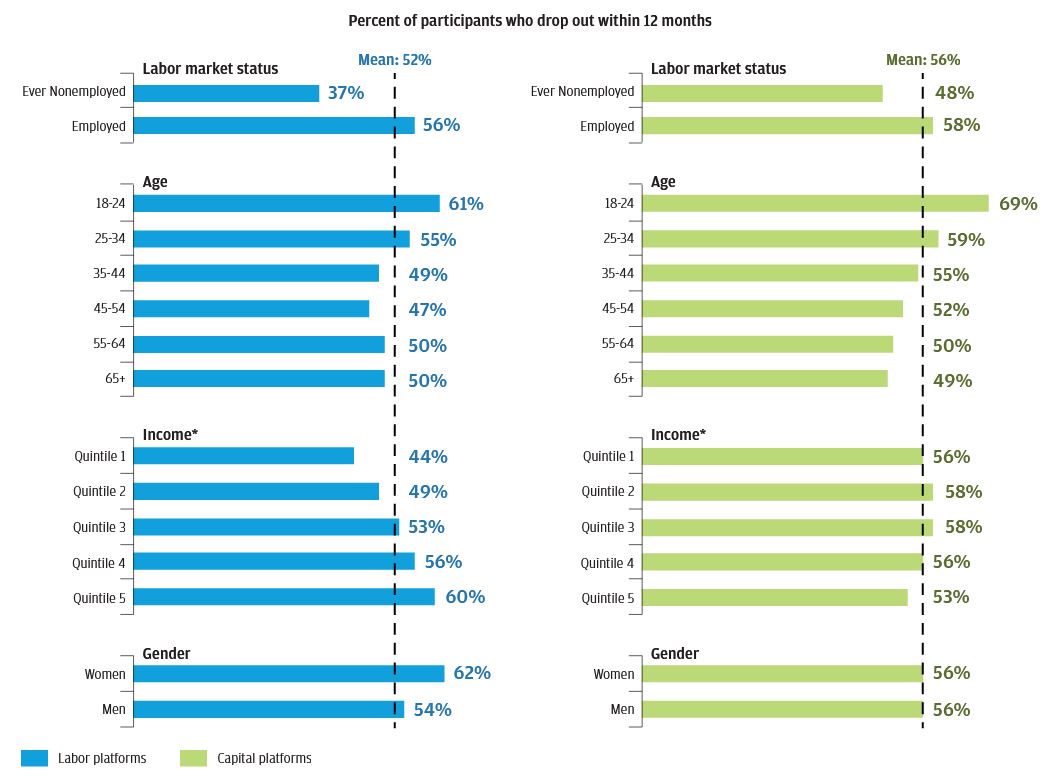

While half of all participants exit the Online Platform Economy within 12 months, some cohorts are more likely to drop out than others. On labor platforms, participants with more stable non-platform employment and higher incomes as well as younger participants (34 and under) are more likely to exit within a year (Figure 11). Younger participants and those with more stable employment are more likely to drop out on capital platforms. For the groups that remain attached to online platforms for more than a year, in particular those with lower incomes and who experienced at least one month of nonemployment over this time frame, platforms provide a vital source of additional income, which we document below.

* Quintile 1: <$30,600, Quintile 2: $30,600-$44,800, Quintile 3: $44,800-$59,000, Quintile 4: $59,000-$84,900, Quintile 5: >$84,900

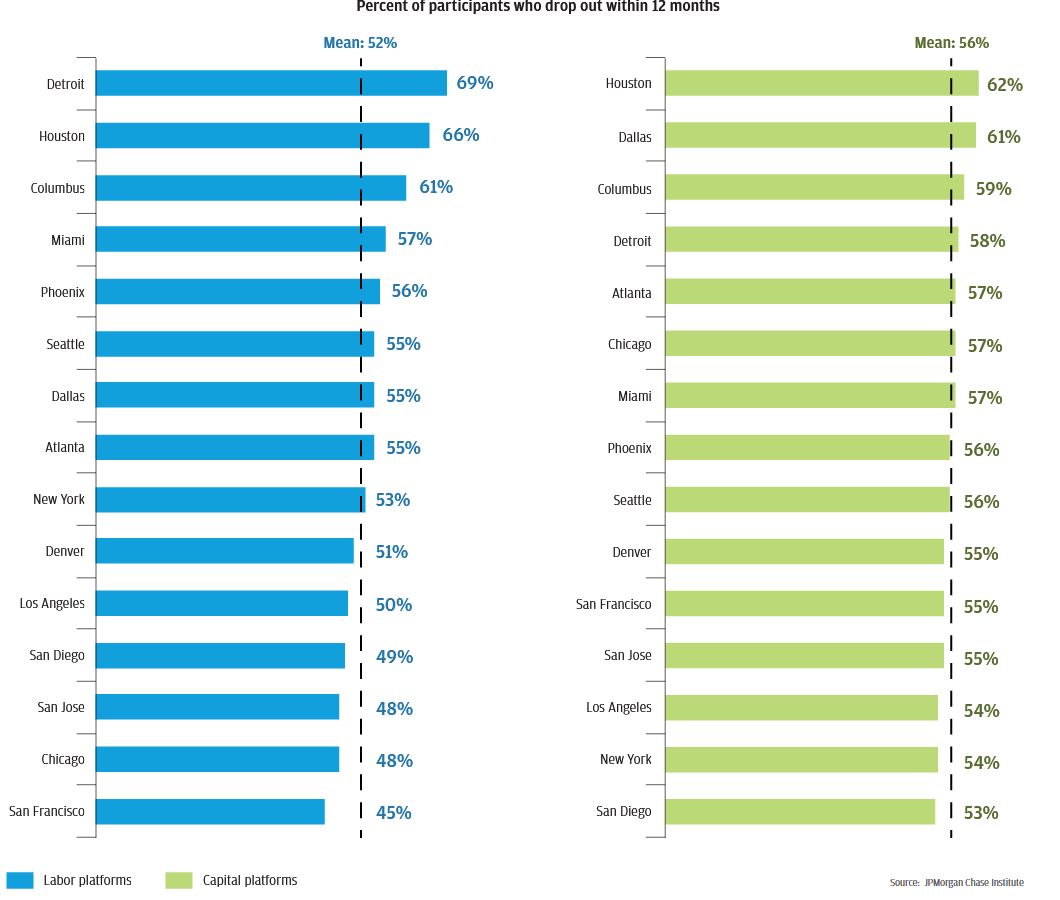

There was wide dispersion in dropout rates across cities on labor platforms but little variation in dropout rates on capital platforms (Figure 12). On labor platforms, the percent of people who drop out of labor platforms within 12 months ranged from 69 percent in Detroit to 45 percent in San Francisco. Recalling Figure 4, cities with lower exit rates also typically have higher levels of participation and lower levels of participation growth. For example, in San Francisco and San Jose, where many platform companies are headquartered and their services were first offered, participation rates are relatively high while both turnover rates and participation growth are relatively low. Part of this relationship is likely mechanical—it is not surprising that participation levels are higher where exit levels are lower. However, it might also suggest that exit rates could decline in cities as labor platform markets mature.

Previously we documented that lower-income individuals were more likely to participate in labor platforms than higher-income individuals, and that they were also more reliant on their labor platform income (JPMorgan Chase Institute, 2016b). As of June 2016, this continues to be the case—0.6 percent of individuals in the lowest income quintile earned income from labor platforms compared to 0.5 percent for the sample as a whole (see Appendix Figures 17-19 for rates of participation and reliance for all demographic groups). We also find that their platform careers are more persistent: 44 percent of participants in the lowest income quintile stopped accessing platform income within 12 months compared to 53 percent of middle income participants and 60 percent in the highest income quintile. The same relationship holds for the nonemployed, among whom participation is more prevalent (Figure 17), reliance is higher (Figure 18), and turnover is lower (Figure 11), than among those with stable jobs or who were employed as of June 2016.

A different pattern exists, however, among the youngest labor platform participants (those ages 18 to 24). Although they have the highest participation rates—1.0 percent on labor platforms and 0.4 percent on capital platforms as of June 2016—they are among the least reliant on platform income, and their careers are particularly short-lived: 61 percent drop out of labor platforms and 69 percent drop out of capital platforms within one year. The only other participants with a higher exit rate on labor platforms are women (62 percent).

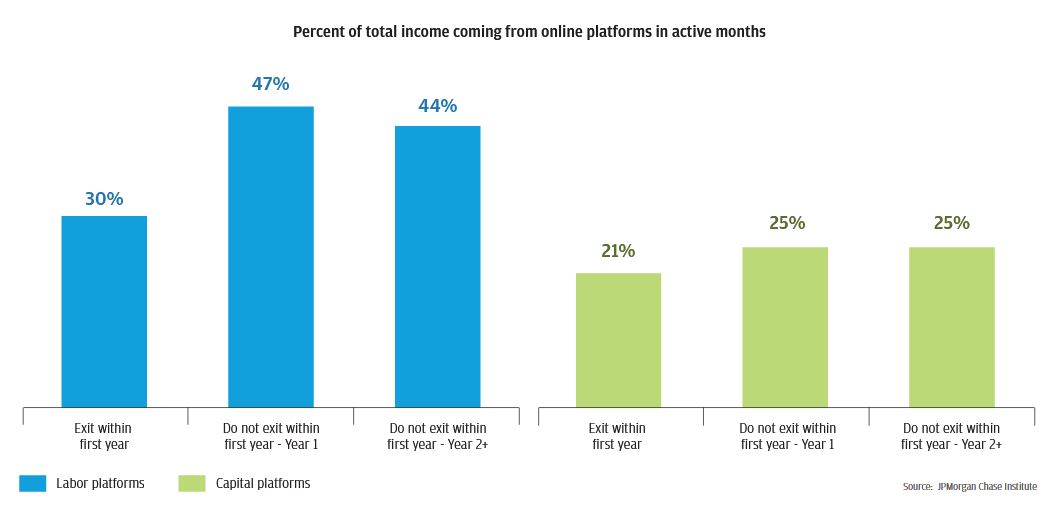

We also examine the relationship between initial reliance on platform income and continued attachment (Figure 13). In the first 12 months of their platform career, we observe that participants who persist on platforms beyond the first year are also more reliant on it in active months than those who drop out within one year: platform income represents 47 percent of income in active months for those who remain in the Online Platform Economy compared to 30 percent for those who drop out.

This difference is also present on capital platforms, though to a lesser extent. For capital platform participants platform income represents 25 percent of income in active months for those who remain in the Online Platform Economy compared to 21 percent for those who drop out.

The degree to which these persistent participants rely on platform income is also consistent throughout their career. For these participants—many of whom are potentially the most economically vulnerable (those with the lowest incomes and who experienced at least one month of nonemployment)—the Online Platform Economy has provided a substantial fraction of their income for an extended period of time.

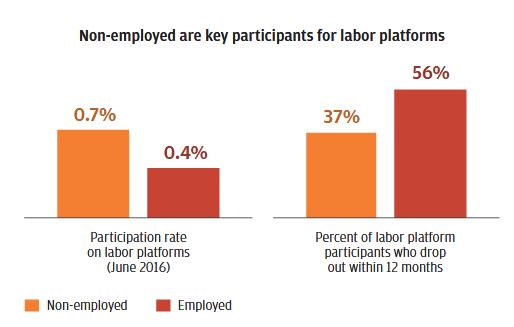

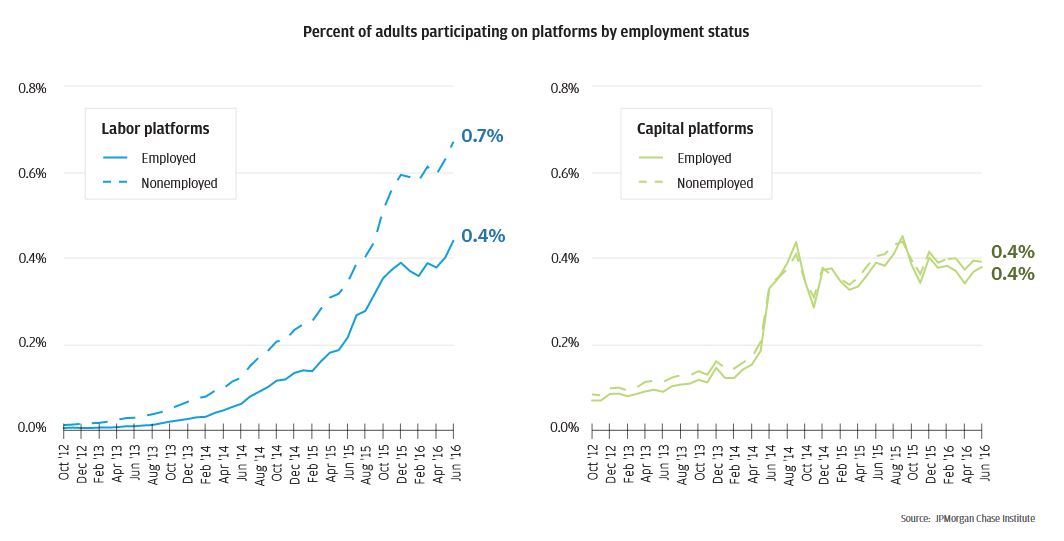

Adults without a non-platform job participate at higher rates on labor platforms than those with earnings from another job (Figure 14). In June 2016, 0.7 percent of nonemployed adults earned income from labor platforms, compared to 0.4 percent of employed adults. Participation rates among different groups with different employment statuses were the same (0.4 percent) on capital platforms.

As of June 2016, 49 percent of labor platform participants and 39 percent of capital platform participants were not employed (Figure 15). 15 As was noted in Finding Four, in addition to participating at higher rates, participants who are not employed have longer platform careers than those who are employed. These data points are consistent with the observation that labor platform participants tend to use platform income to smooth over dips in non-platform income. The Online Platform Economy, therefore, represents a relatively accessible and flexible source of additional income for those who might need it most.

The gap in participation rates on labor platforms between the nonemployed and the employed widened in the fourth quarter of 2015 and the first half of 2016. In fact, the growth in participation among the employed was slower over this nine month period than in previous months, while participation among the nonemployed more closely tracked its previous trajectory. This implies that much of the growth in labor platform participation during these months came from the nonemployed. Moreover, as the traditional labor force strengthens, as a result of both falling unemployment and increases in real wages , labor supply in the Online Platform Economy might weaken (Furman, 2016).

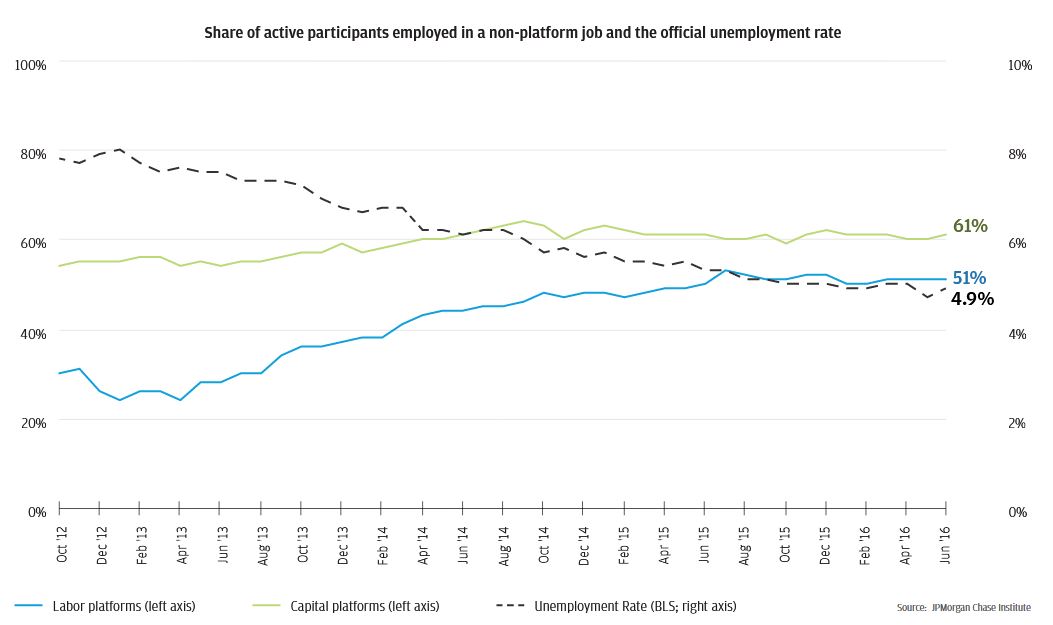

The fraction of participants holding a non-platform job increased on both labor and capital platforms since October 2012 as the unemployment rate dropped (Figure 15). The fraction of labor platform participants with a non-platform job increased from a low of 24 percent in January 2013 to 51 percent in June 2016 while the official unemployment rate fell from 8.0 percent to 4.9 percent over the same period. 16 The fraction of capital platform participants with a non-platform job increased more modestly from a low of 54 percent in October 2012 to 61 percent in June 2016. This suggests that labor platform participation might be more sensitive to conditions in the traditional labor market than capital platform participation. 17

In June 2016, 0.9 percent of adults earned income from the Online Platform Economy, including 0.5 percent on labor platforms and 0.4 percent on capital platforms. With labor platforms participation still doubling year-over-year, some have called this platform work the “future of work.” However, participation growth on both labor and capital platforms has peaked. Our findings presented here suggest several important dimensions of how growth has slowed:

These trends underscore that growth in online platform participation is highly dependent on attracting new participants or increasing the attachment of existing participants. The flexibility afforded by platform work alone might not be sufficient to continue to attract and engage participants on existing terms. In addition to these factors, autonomous vehicles, and automation more generally, could eliminate some labor platform opportunities for independent workers. Efforts to make independent work more sustainable and supportive for workers across all types of platforms might be necessary to realize continued growth.

High participant turnover is an important consideration in designing those support systems. For example, many policy makers are exploring whether workers’ benefits could become more portable. In a world in which benefits are accrued on a pro-rated basis by workers from an array of employers, as some have suggested, the administrative burden associated with high turnover could be substantial if enrollment and re-enrollment are manual processes (Rolf, et al., 2016). Automating these processes might be an important priority if portable benefits aim to be truly universal and cover all workers. Otherwise minimum eligibility requirements might be necessary to limit the administrative burden of managing short-lived participants.

While growth in the Online Platform Economy might be slowing, it is a small part of the broader phenomenon of an increased prevalence of alternative work arrangements. Katz and Kruger (2016) show that the share of workers in alternative arrangements, including independent contractors or freelancers, has increased from 10.7 percent in 2005 to 15.8 percent in 2015. The Online Platform Economy provides an important window into the participation and growth dynamics of independent work more generally.

Bensinger, Greg. 2016. “Grocery-Delivery Startup Instacart Cuts Pay for Couriers.” Wall Street Journal . http://www.wsj.com/articles/grocery-delivery-startup-instacartcuts-pay-for-couriers-1457715105

Bureau of Labor Statistics. 2016. “Employee Tenure in 2016.” http://www.bls.gov/news.release/pdf/tenure.pdf

Census Bureau. 2016. “Quarterly Retail E-Commerce Sales: 2nd Quarter 2016.” https://www.census.gov/retail/mrts/www/data/pdf/ec_current.pdf

Farrell, Diana and Greig, Fiona. 2016. “Paychecks, Paydays, and the Online Platform Economy.” JPMorgan Chase Institute. https://www.jpmorganchase.com/corporate/institute/document/jpmc-institute-volatility-2-report.pdf

Furman, Jason. 2016. “The Employment Situation in September.” Council of Economic Advisers. https://www.whitehouse.gov/blog/2016/10/07/employment-situation-september

Griffeth, Rodger W., Hom, Peter W., and Gaertner, Stefan. 2000. “A Meta-analysis of Antecedents and Correlates of Employee Turnover: Update, Moderator Tests, and Research Implications for the Next Millennium.” Journal of Management 26(3): 463-488. http://www. sciencedirect.com/science/article/pii/S014920630000043X

Hall, Jonathan and Krueger, Alan. 2015. “An Analysis of the Labor Market for Uber’s Driver-Partners in the United States.” Princeton University, Industrial Relations Section Working Papers 5 8 7. http://arks.princeton.edu/ark:/88435/dsp010z708z67d

JPMorgan Chase Institute. 2016a. “The Online Platform Economy: What is the Growth Trajectory?” https://www.jpmorganchase.com/corporate/institute/insight-online-platform-econ-growth-trajectory.htm

JPMorgan Chase Institute. 2016b. “The Online Platform Economy: Who earns the most?” https://www.jpmorganchase.com/corporate/institute/insight-online-platform-econ-earnings.htm

Katz, Lawrence and Krueger, Alan. 2016. “The Rise and Nature of Alternative Work Arrangements in the United States, 1995-2015.” National Bureau of Economic Research Working Papers 2 26 67. http://www.nber.org/papers/w22667

KPMG and CB Insights. 2016. “Venture Pulse Q3 2016: Global Analysis of Venture Funding.” https://assets.kpmg.com/content/dam/kpmg/xx/pdf/2016/10/venture-pulse-q3-2016-report.pdf

Manyika, James, Lund, Susan, Bughin, Jacques, Robinson, Kelsey, Mischke, Jan, and Mahajan, Deepa. 2016. “Independent Work: Choice, Necessity, and the Gig Economy.” McKinsey & Company . http://www.mckinsey.com/global-themes/employment-and-growth/independent- work-choice-necessity-and-the-gig-economy

Mims, Christopher. 2016. “This Tech Bubble Is Bursting.” Wall Street Journal . http://www.wsj.com/articles/this-tech-bubble-is-bursting-1462161662

Rolf, David, Clark, Shelby, and Bryan, Corrie Watterson. 2016. “Portable Benefits in the 21st Century: Shaping a New System of Benefits for Independent Workers.” The Aspen Institute Future of Work Initiative . https://dorutodpt4twd.cloudfront.net/content/uploads/2016/07/Portable_Benefits_final2.pdf

SherpaShare. 2015. “The top demographic trends of the on-demand workforce.” https://www.sherpashare.com/share/the-top-demographic-trends-of-the-on-demand-workforce/

Siddiqui, Faiz. 2016a. “Metro’s Loss is Rideshares’ Gain.” Washington Post . https://www.washingtonpost.com/news/dr-gridlock/wp/2016/09/07/metros-loss-is-rideshares-gain/?tid=a_inl

Siddiqui, Faiz. 2016b. “D.C.-based Split will discontinue rideshare service, citing market ‘saturation’.” Washington Post . https://www. washingtonpost.com/news/dr-gridlock/wp/2016/09/27/d-c-based-split-will-discontinue-rideshare-service-citing-market-saturation/

Wang, Selina. 2016. “Uber Drivers Strike to Protest Fare Cuts in New York City.” Bloomberg . https://www.bloomberg.com/news/articles/2016-02-01/uber-drivers-plan-strike-to-protest-fare-cuts-in-new-york-city

Farrell, Diana and Greig, Fiona. 2016. "The Online Platform Economy: Has Growth Peaked?" JPMorgan Chase Institute.

JPMorgan Chase & Co.'s website terms, privacy and security policies don't apply to the site or app you're about to visit. Please review its website terms, privacy and security policies to see how they apply to you. JPMorgan Chase & Co. isn't responsible for (and doesn't provide) any products, services or content at this third-party site or app, except for products and services that explicitly carry the JPMorgan Chase & Co.