We no longer support this browser. Using a supported browser will provide a better experience.

Please update your browser.

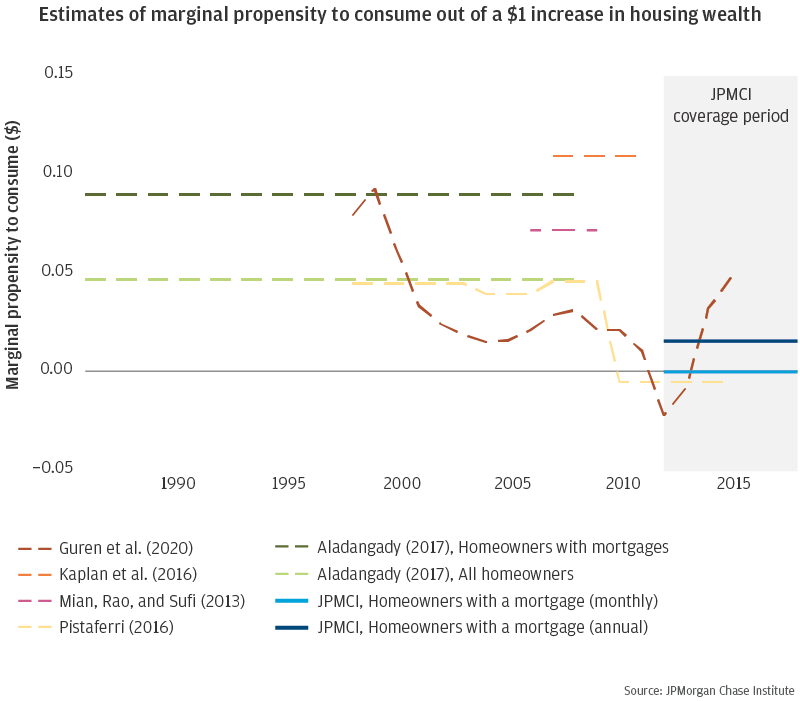

Roughly two-thirds of families in the U.S. own a home. Rising home prices, and therefore housing wealth, can fuel household consumption. As such, the housing market can have a significant impact on the broader economy. From the late 1990s up to the Great Recession, estimates of the marginal propensity to consume (MPC) out of housing wealth range from approximately 4 cents to 9 cents, and studies covering the Great Recession period have found MPCs as high as 11 cents.1 However, evidence of slower-than-expected consumption and GDP growth in combination with relatively low levels of home equity extraction after the Great Recession suggest that the housing wealth effect may be much smaller after the financial crisis than for prior periods. Indeed, some recent studies suggest that the MPC may be as low as zero, but these studies do not provide precise causal estimates.

In this report, we answer the following research question: What was the household consumption response to the 50 percent increase in housing wealth in the post-Great Recession period? We link de-identified banking data, including transaction-level deposit account and credit card data, to loan-level mortgage data to estimate the MPC out of housing wealth for the period between 2012 and 2018. Our large sample and direct measure of consumption allow us to derive more precise MPC estimates than otherwise available.

The marginal propensity to consume is the proportion of an increase in income or wealth that a consumer chooses to spend on goods and services rather than save.

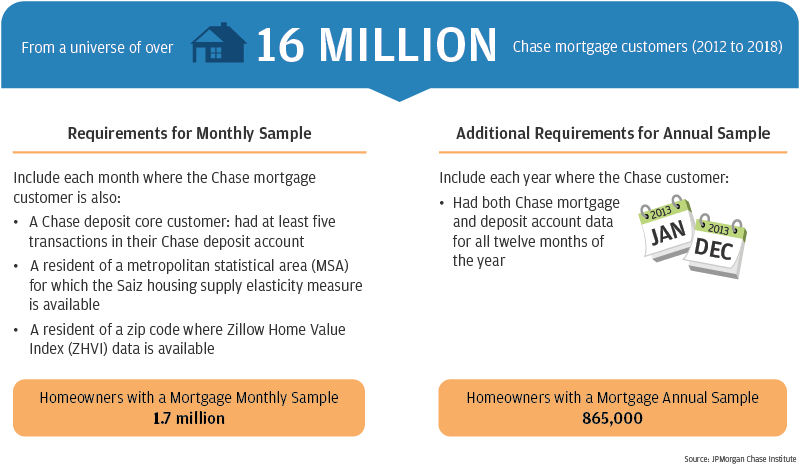

From a universe of over 16 million Chase mortgage customers between 2012 and 2018, we created a sample of 1.7 million customers who had both a Chase mortgage and Chase deposit account during that period and who fulfilled other criteria described above. Our loan-level mortgage data allow us to observe details of each homeowner’s loan (e.g., current levels of equity). In a robustness check, we also examined a sample of over 5 million Chase credit card customers who are likely to be homeowners according to information on their credit card application. Following similar studies that estimate housing wealth effect MPCs for prior periods, we use an instrumental variables strategy with housing supply elasticity as the instrument to derive causal estimates.

We find that the MPC out of increasing housing wealth from 2012 to 2018 is 0 cents for our monthly sample and 1.6 cents for our annual sample, both of which are significantly lower than most estimates in the literature for prior periods. Studies find MPCs as high as 11 cents for the period from the late 1990s through the Great Recession.

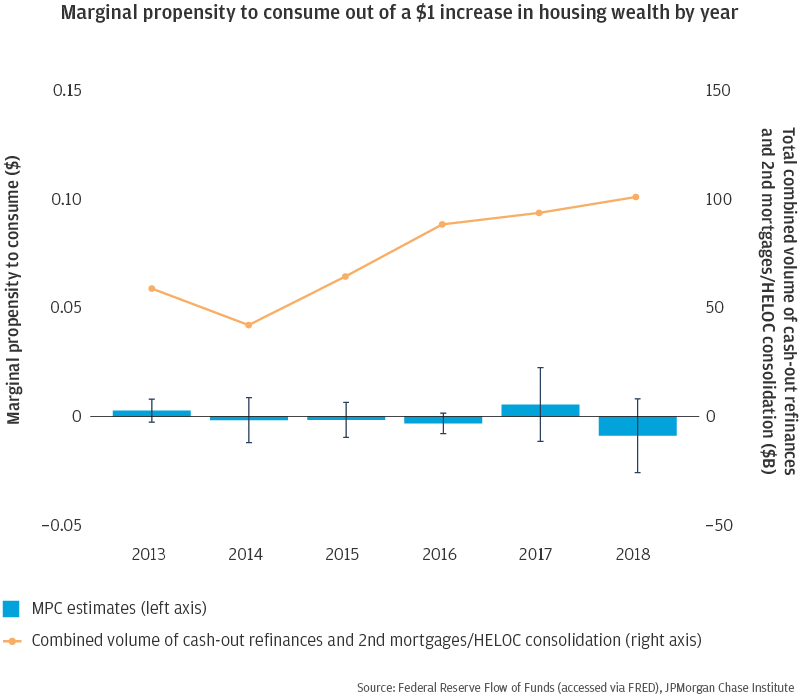

For each year between 2013 and 2018, our estimated housing wealth effect MPC is both very small and statistically insignificant, implying the same MPC of zero for each year. This is consistent with data on equity extraction, which show that for the latter years in the range, equity extraction activity increased slightly but remained far below the historically high levels seen prior to the Great Recession.

Implications

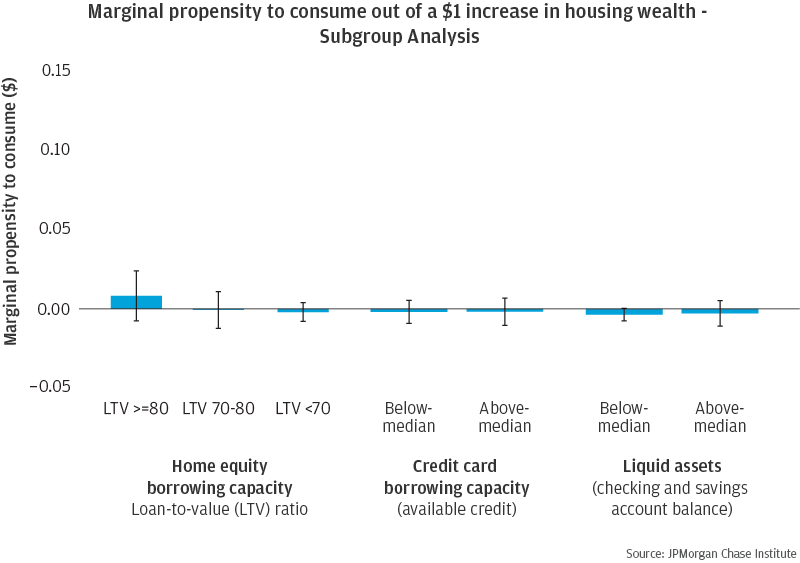

How do we reconcile the much smaller MPC out of housing wealth in the post-Great Recession period with a larger MPC during the preceding periods? We find that the volume of equity withdrawal in the post-Great Recession period was much lower than during the housing boom. Research suggests there are both demand and supply factors at play. After the financial crisis, a larger share of equity became concentrated in the hands of older and less credit-constrained borrowers who tend to have a lower demand for equity extraction. At the same time, tightened lending standards have reduced the supply of credit to more credit-constrained mortgage holders who may have greater demand for equity extraction. We contribute new evidence that a lack of demand to borrow against home equity contributed to a low marginal propensity to consume out of housing wealth: even homeowners with more equity (for whom it should be easy to borrow) did not consume more when housing wealth rose.

This research has several implications for policymakers and is particularly relevant as the economy comes to face a severe recession induced by the COVID-19 pandemic. First, homeowners entered the COVID-19 crisis with a substantial amount of illiquid wealth in the form of home equity. Given the importance of cash flow dynamics and liquidity as determinants of consumption and the ability to stay current on housing payments, measures that allow homeowners to preserve or increase liquidity in the face of financial distress, such as through forbearance or maintaining access to this home equity, could provide an important financial cushion. These types of measures carry risks, however, as home prices could depreciate in a recession, eroding the equity position of homeowners—and increased income volatility could make it more difficult for borrowers to meet debt obligations.

Second, a much smaller housing wealth effect diminishes the ability of conventional monetary policy—changes to short-term interest rates—to affect the real economy through the housing market, resulting in lower consumption and GDP growth than policymakers might have expected or hoped to stimulate. Had the housing wealth effect MPC remained at estimated pre-recession levels, we find that consumption and GDP would have been 0.1 to 1.5 percent and 0.1 to 1 percent higher, respectively, in each of the years from 2012 to 2018.2 As such, policymakers may need to lean more heavily on other channels of monetary policy and unconventional measures, as well as fiscal policies that provide households with liquidity during an economic downturn.

JPMorgan Chase & Co.'s website terms, privacy and security policies don't apply to the site or app you're about to visit. Please review its website terms, privacy and security policies to see how they apply to you. JPMorgan Chase & Co. isn't responsible for (and doesn't provide) any products, services or content at this third-party site or app, except for products and services that explicitly carry the JPMorgan Chase & Co.