We no longer support this browser. Using a supported browser will provide a better experience.

Please update your browser.

For many, owning a home is a vital part of the American dream. To promote homeownership, many policies have been enacted over the past 80 years, and the mortgage has become the financing instrument of choice for most home buyers.

The aftermath of the Great Recession was a particularly difficult period for many homeowners with a mortgage. The steep decline in home prices meant that by the end of 2011 many borrowers were “underwater”—they owed more on their mortgage than their home was worth. During the same period, the unemployment rate nearly doubled and delinquency rates on residential mortgages spiked. In response, various mortgage modification programs were introduced to help homeowners struggling to make their monthly mortgage payments remain in their homes. In this JPMorgan Chase Institute report, we analyzed homeowners who received a mortgage modification to better understand the impact of modifications on homeowner behavior.

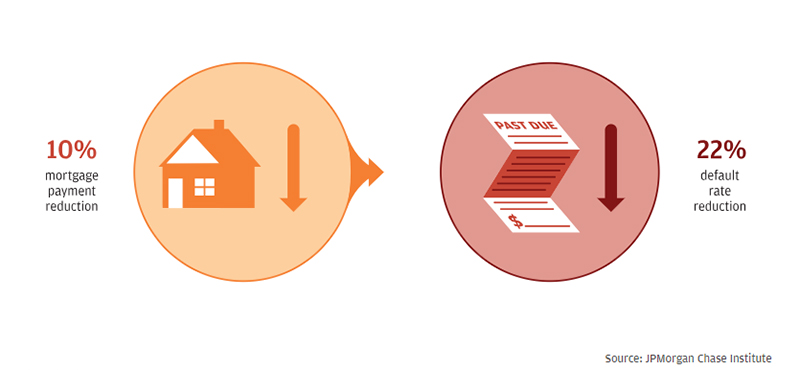

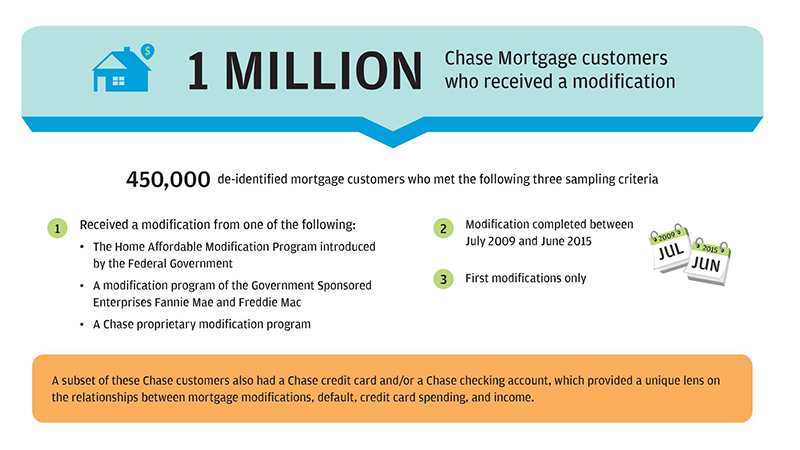

Using mortgage, credit card, and deposit account data from a de-identified sample of Chase customers, we investigated the relative importance of different features of mortgage modification programs. In particular, we studied the impact of reductions in monthly mortgage payments and principal on default and consumption.

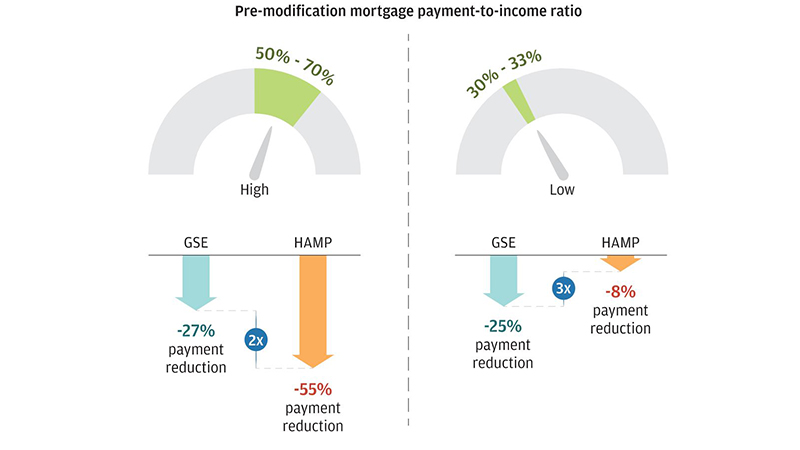

Borrowers with similar payment burdens (as measured by pre-modification mortgage payment-to-income ratio, or PTI) received considerably different payment reductions depending on the modification they received:

*HAMP refers to the Home Affordable Modification Program introduced by the Federal Government and the GSE program refers to the proprietary modifications offered by the Government Sponsored Enterprises Fannie Mae and Freddie Mac.

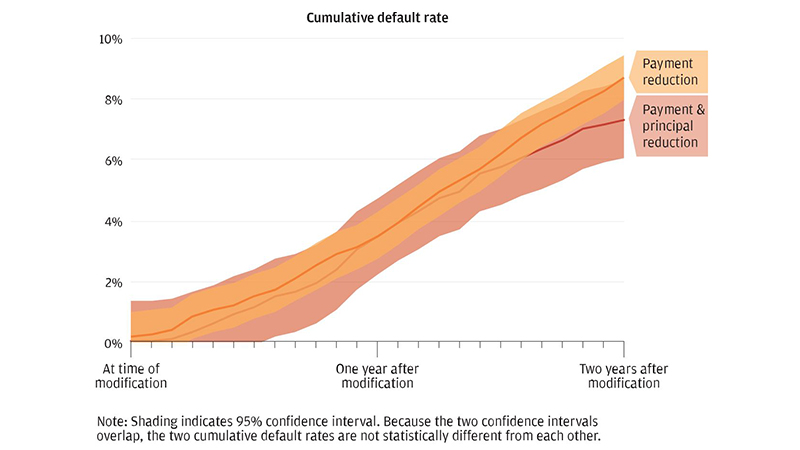

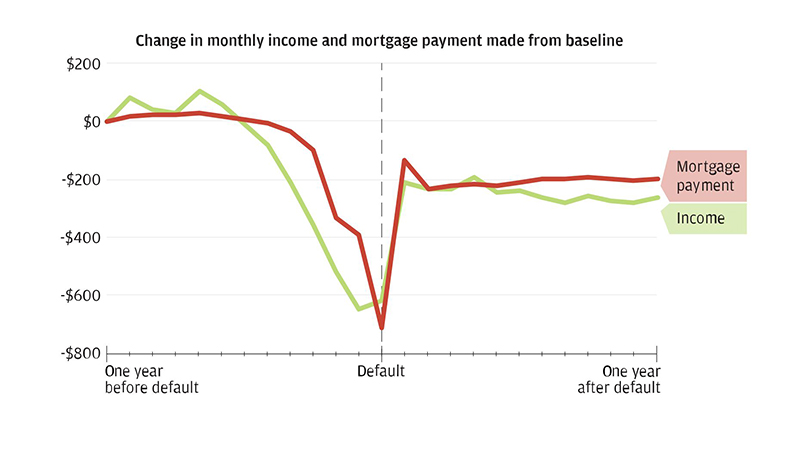

There was no difference between the post-modification default rates of borrowers who received principal plus payment reduction and borrowers who received only payment reduction. This finding suggests that “strategic default” was not the primary driver of default decisions for these underwater borrowers, meaning that they were not defaulting simply because they owed more on their mortgage than their house was worth.

Conclusion

In this report, we measured the impact of mortgage payment and principal reduction on default and consumption. Our results have implications for both housing policy and monetary policy.

Our findings suggest that mortgage modification programs that are designed to target substantial payment reduction will be most effective at reducing mortgage default rates. Modification programs designed to reach affordability targets based on debt-to-income measures without regard to payment reduction will be less effective. Principal focused mortgage debt reduction programs that target a specific LTV ratio but leave borrowers underwater will also be less effective at reducing defaults.

To the extent that a mortgage modification can be considered a re-origination, our findings may have application to underwriting standards as well. The fact that default was correlated with income loss provides evidence that static affordability measures such as debt-to-income ratio were not a good predictor of default. Both high and low mortgage PTI borrowers experienced a similar income drop just prior to default, suggesting that even among those borrowers whose mortgages would be categorized as unaffordable by conventional standards, it was a drop in income rather than a high level of payment burden that triggered default. Therefore, policies that help borrowers establish and maintain a suitable cash buffer that can be drawn down in the event of an income shock or an expense spike could be an effective tool to prevent mortgage default.

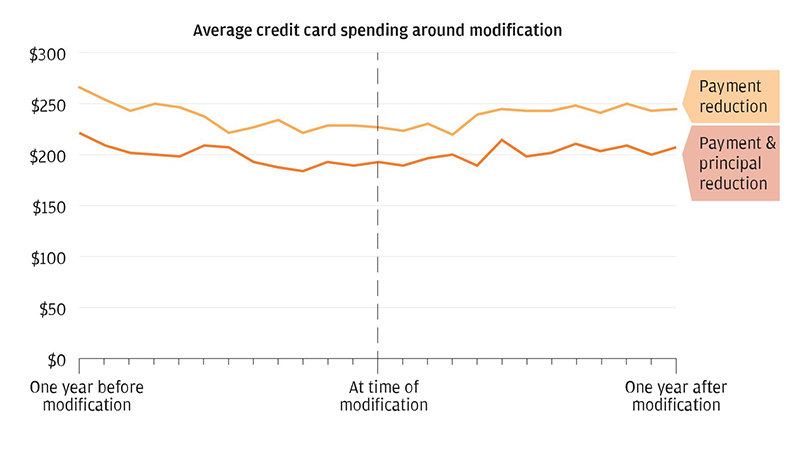

The housing wealth effect is one of the important mechanisms that transmits changes in monetary policy to household consumption. This transmission mechanism relies on accommodative monetary policy leading to higher house prices, and the increase in housing wealth that in turn stimulates consumption. The lack of consumption response from underwater borrowers to principal reductions suggests that the marginal propensity to consume out of housing wealth is nearly zero for these homeowners. For underwater borrowers, the inability to translate increased home equity into liquid resources (e.g., through equity extraction) may nullify the housing wealth effect and thus constrain this transmission mechanism.

JPMorgan Chase & Co.'s website terms, privacy and security policies don't apply to the site or app you're about to visit. Please review its website terms, privacy and security policies to see how they apply to you. JPMorgan Chase & Co. isn't responsible for (and doesn't provide) any products, services or content at this third-party site or app, except for products and services that explicitly carry the JPMorgan Chase & Co.