We no longer support this browser. Using a supported browser will provide a better experience.

Please update your browser.

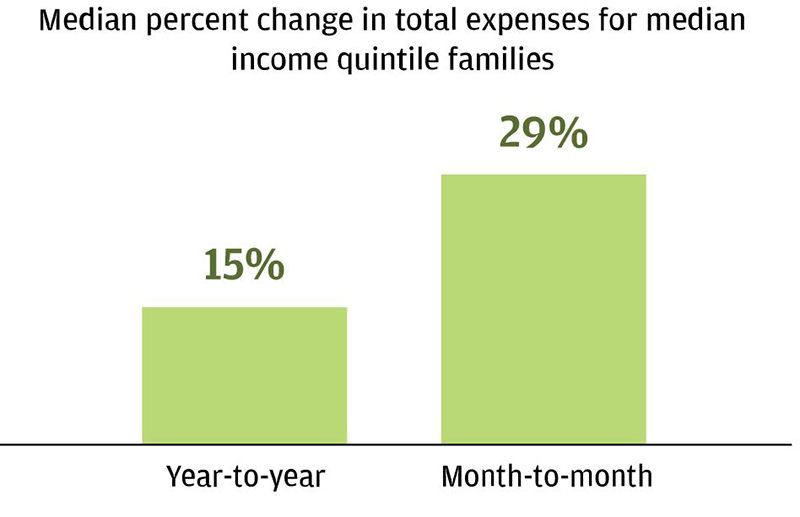

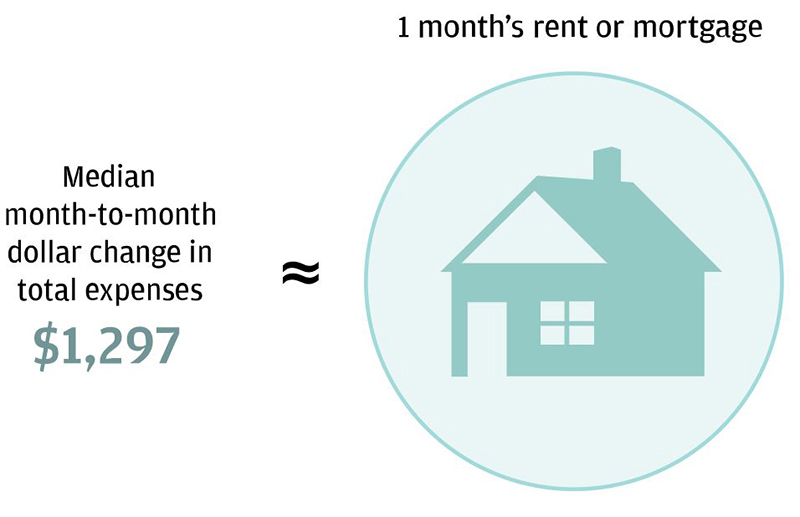

Americans across the income spectrum experience tremendous income and expense volatility, and this volatility has been on the rise. This volatility tests the financial resilience of American families. In Weathering Volatility, we estimated that median-income families needed $4,800 in liquid assets to weather 90 percent of the income and expense volatility observed, but that they had only $3,000—a shortfall of $1,800. In Paychecks, Paydays, and the Online Platform Economy we documented that most income volatility stems from labor income and, specifically, variation in take-home pay within a job rather than job transitions.

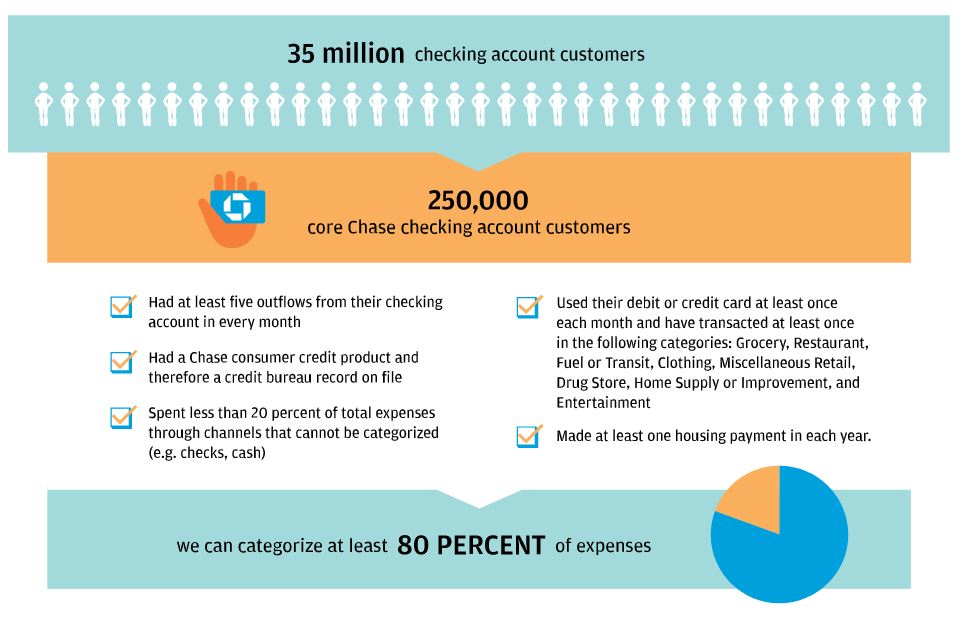

In this report, the JPMorgan Chase Institute assembled a de-identified data asset of nearly 250,000 Chase customers between 2013 and 2015 in order to study how consumers’ expenses vary over time and how their financial behavior changes when faced with extraordinary payments. This high-frequency panel of family finances—weighted to represent the age and income distribution of the nation—provides a first ever look into the components of expense volatility based on real financial transactions and the changes to family income, expenses, assets, and liabilities that coincide with extraordinary medical payments.

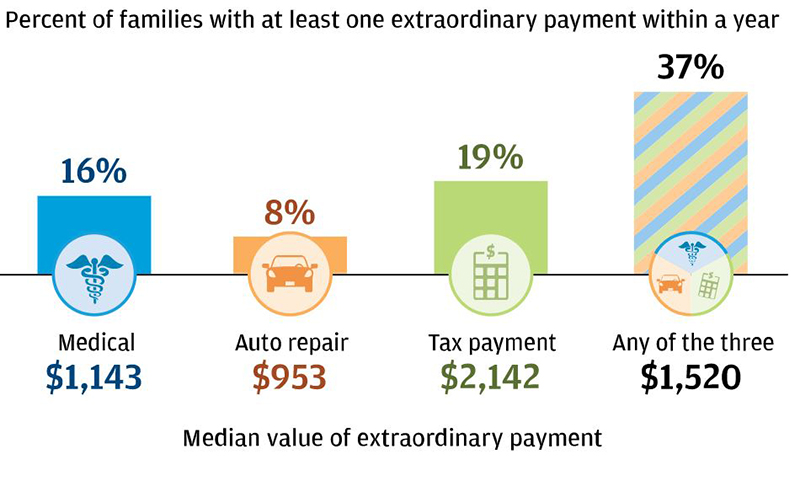

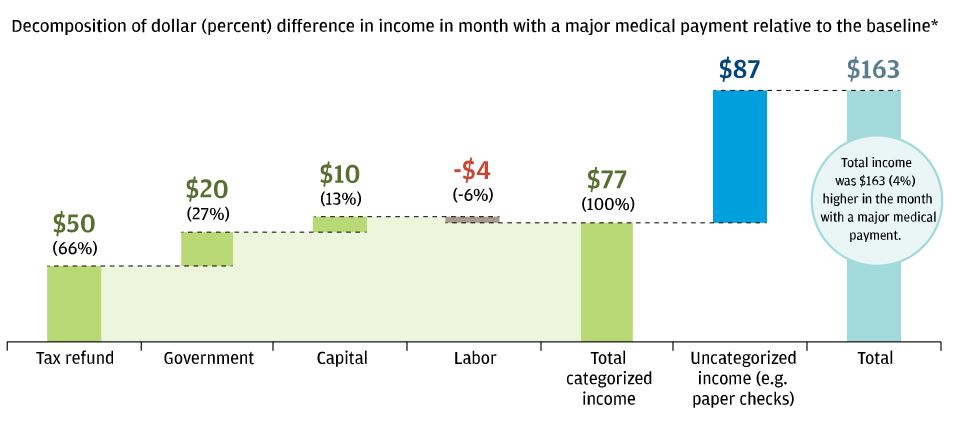

Extraordinary medical payments were more likely to occur in months with higher income. Total income was $163 or 4 percent higher in months with a major medical payment. The income increase stemmed mostly from tax refunds and not labor income and was still small in magnitude compared to the mean medical payment of $2,089.

From a universe of 35 million checking account customers, we assembled a de-identified data asset comprised of roughly 250,000 core Chase customers for whom we could categorize at least 80 percent of expenses. These families met the following five sampling criteria:

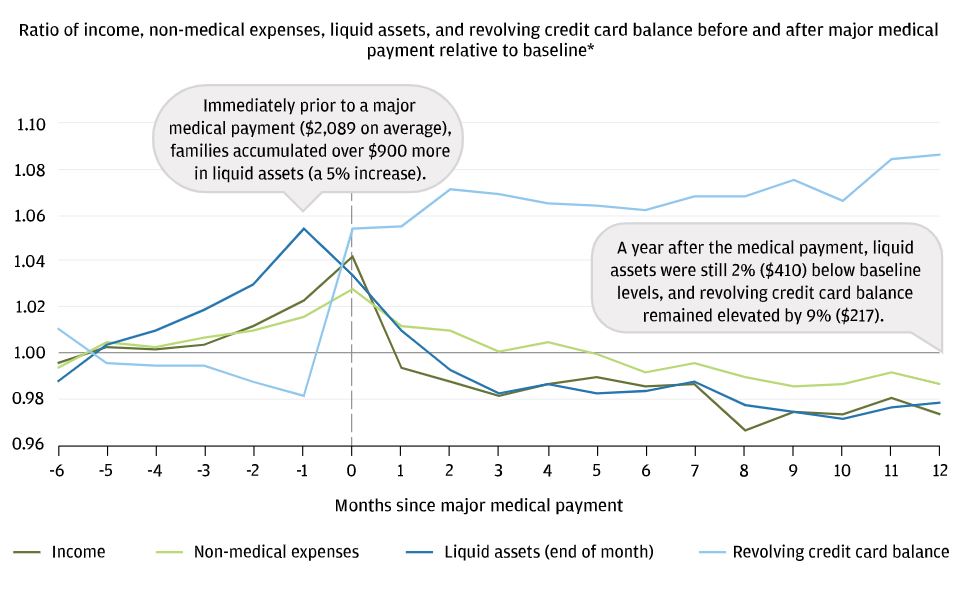

These findings highlight the critical role liquid assets play in managing expense spikes and the need for policies and solutions to promote emergency savings. While many families experienced an increase in income in the month in which they made a major medical payment, liquid assets were the primary source of funding to cover the medical payment. Our evidence also underscores the connections between financial health and physical health. First, the timing of medical payments was linked to ability to pay. Families may have delayed either medical treatment or payment of their medical bill until they were able to pay. The second link is that major medical payments were associated with lower income, non-medical expenses, and liquid assets and higher credit card debt a year later. This highlights the reality that families are not fully insured against the economic consequences of major health events. Older families in particular could benefit from more customized solutions as they exhibited a greater range in income and expense volatility and were also more likely to make major medical payments. More broadly, better solutions could help families accumulate liquid assets and predict, manage, and afford expense spikes. Integrated, high-frequency data of income, expenses, assets, and liabilities shed new light on expense volatility and how behavior changes with this volatility. This is critical to improving policies and solutions to strengthen the financial resilience of American families.

JPMorgan Chase & Co.'s website terms, privacy and security policies don't apply to the site or app you're about to visit. Please review its website terms, privacy and security policies to see how they apply to you. JPMorgan Chase & Co. isn't responsible for (and doesn't provide) any products, services or content at this third-party site or app, except for products and services that explicitly carry the JPMorgan Chase & Co.